Precious Metals May Outlook: After U.S.-Iran Conflict Concerns Eased, Will Funds Flow Back to Gold and Silver?

TradingKey - Since April, the precious metals market has continued the weak trend from March. Spot gold fell by nearly 2% in April, and spot silver once dropped below the $70 mark.

Previously, on April 17, Iran announced the temporary opening of the Strait of Hormuz, sending spot gold surging to $4,887 per ounce and silver jumping above $82; 24 hours later, Iran blocked the strait again, and gold prices lost the $4,800 level.

On April 27, Iranian Foreign Minister Araghchi traveled to Pakistan again to submit ceasefire conditions, but U.S.-Iran negotiations remain deadlocked, with disagreements over Hormuz transit rights and nuclear talks still serving as core obstacles.

Against the backdrop of a fluctuating geopolitical narrative, a more central question faces investors: as "conflict concerns" recede from the market focus, what factors will actually determine the return of capital to gold and silver?

Changing strategic logic; geopolitical premiums dissipate.

Since the outbreak of the US-Iran conflict on February 28, precious metals trading has gradually shifted from systemic liquidity demand-driven trading to trading based on negotiation outcomes.

On April 17, the day Iran announced the reopening of the Strait of Hormuz, the United States immediately imposed a strict maritime blockade after the first round of negotiations in Islamabad ended without result; in response, Iran closed the strait again on the 18th, with 35 vessels turning back within 36 hours while attempting to exit.

Now, as May approaches, marginal changes in the geopolitical narrative merit attention. On the 26th, Araghchi submitted ceasefire terms to Pakistan focusing on practical issues such as a new legal regime for the Strait of Hormuz and the lifting of the maritime blockade. Meanwhile, the UK and France are advancing plans to restore navigation in the strait at a multilateral military planning meeting, while British and American leaders discussed the urgency of restoring passage in a call.

These developments indicate that the maneuvering between the two sides is shifting toward a regional standoff.

When geopolitical maneuvering reaches a critical point of equilibrium, gold prices lack geopolitical catalysts in the short term, and the market often begins to price in the trajectory of real interest rates and the U.S. dollar as uncertainty subsides.

Medium-term structural support remains, but capital exhibits structural divergence.

Market analysis suggests that the primary driver of the current gold price volatility is not geopolitical risk itself, but rather a liquidity shock.

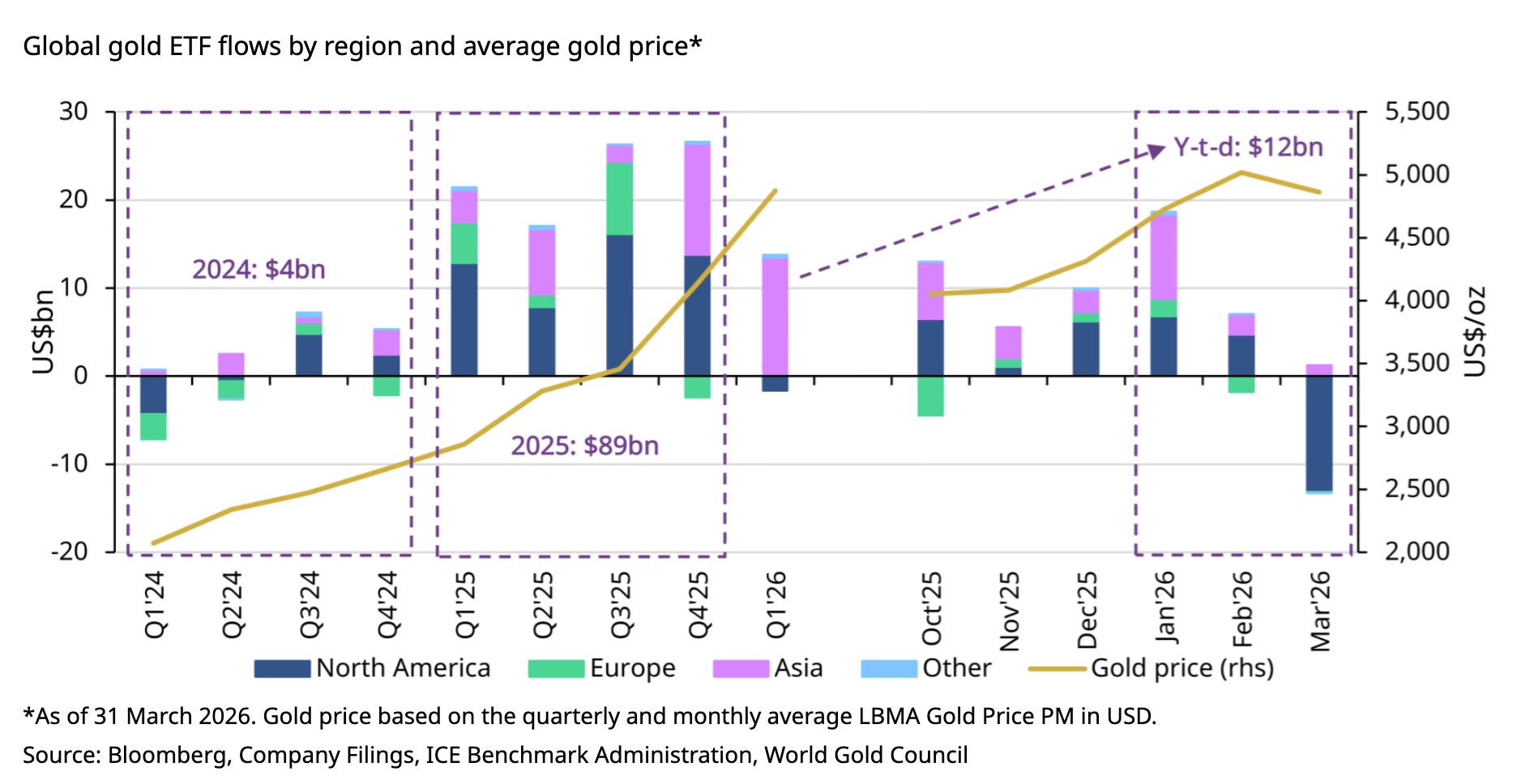

A massive influx of speculative and leveraged funds since the second half of last year staged a concentrated exit as geopolitical risks escalated. This, combined with some investors selling gold to cover liquidity gaps, collectively amplified market volatility. Bloomberg Intelligence data shows that commodity ETFs have suffered record outflows of $11 billion since March, with gold ETF redemptions exceeding $7 billion and silver ETF outflows totaling approximately $1.4 billion.

[Gold ETFs saw record selling in March, Source: World Gold Council]

However, as short-term capital retreated, World Gold Council data showed that global central banks made net purchases of 863 tonnes in 2025 and 215 tonnes in the first quarter of 2026, with the People's Bank of China increasing its holdings for 17 consecutive months. Amid the wave of de-dollarization, continued accumulation by central banks in emerging markets such as China has established long-term bottom support for gold prices.

Short-term outflows do not signify a total capital exodus. For long-term allocation capital, a genuine "easing of concerns" may represent a window for re-pricing rather than a signal of a fundamental reversal in logic.

Liquidity retreats as interest rate anchoring potentially becomes the dominant trade.

Although Goldman Sachs maintains its $5,400 price target for the end of 2026, current spot precious metal trends indicate that the market still prices spot gold and silver as risk assets; when geopolitical risks escalate further, spot gold and silver often come under downward pressure, which runs contrary to the safe-haven logic previously recognized by capital.

TradingKey analysis suggests that the partial failure of the safe-haven logic stems from the excessive preceding rally. Short-term market capital previously adopted a "buy first, see later" approach before the outbreak of geopolitical conflicts, aggressively increasing positions in safe-haven precious metal assets via ETFs and other vehicles, pushing gold and silver prices to heights that their fundamentals could not support. Essentially, the previous gains have already fully priced in any potential future escalation of geopolitical risks.

Consequently, the outbreak of the U.S.-Iran conflict instead helped "buy the rumor, sell the news" trading become the market mainstream.

In April, as safe-haven sentiment gradually dissipated, the sole fundamental premium for precious metals was also eroded. Analysts believe the primary variable that could reverse the bearish sentiment for precious metals in May is a simultaneous decline in U.S. Treasury yields and the dollar, particularly if U.S. inflation, employment, or consumption data show clear cooling.

The fundamental pricing anchor for gold at this stage is actually U.S. real interest rates. Currently, as Warsh is set to become Fed Chair, his recent hawkish policy signals during hearings have made market expectations for the Fed's rate path more cautious, driving continued resilience in the dollar.

This context means that even if some progress is made in U.S.-Iran negotiations in May, a full return of allocation-oriented capital still awaits a clearer "dovish pivot" in Fed policy. In the coming months, the U.S.-Israel-Iran conflict is likely to reach a phased resolution, while the new Fed Chair will outline a new monetary policy path; these two variables will collectively determine the next direction for precious metals.

Divergence in Gold and Silver Performance

It is worth noting that even if capital returns, the pace of inflows for gold and silver may differ significantly.

Silver’s high exposure to industrial demand means slowing economic growth could directly weigh on its performance. Lacking the fundamental support of central bank purchases, its fundamentals remain relatively fragile. In contrast, gold benefits from persistent net central bank buying, de-dollarization trends, and physical investment, demonstrating far greater resilience. Consequently, gold’s strategic allocation value remains firm for May's positioning, while silver requires more substantive support from industrial demand to initiate a sustained trend higher.

Over the medium to long term, the structural case for precious metals remains solid. The de-dollarization wave remains a primary market theme, central bank buying continues, and the macro backdrop of elevated U.S. debt and tepid growth persists. Therefore, gold’s role as a strategic allocation asset remains unchanged.

In the short term, however, the geopolitical narrative's shift from extreme uncertainty toward 'brinkmanship' and the lack of clarity regarding the policy path after Warsh succeeds Powell suggest that capital inflows are unlikely to take the form of a 'one-way rally.'

With the Fed's leadership transition in May and progress in mid-term U.S.-Iran negotiations, the market will undergo a period of repricing as it absorbs these multiple developments.

Recommended Articles