Match Group (MTCH): Cautiously Swiping Right on It

Investment Thesis

TradingKey - Currently the market dislikes dating app stocks like Match and Bumble, and for a reason. The user engagement has been declining for a while, and the stock has gone nowhere in the last two years. However, Match Group still has tools to change this due to the following: 1) Dominant market position with several well-known brands; 2) Hinge is still in a good momentum; 3) Overseas usage of dating apps is far from mature; 4) Match has room to increase marketing spending; 5) The debt situation is stable.

.jpg)

Source: TradingView

Company Description

MTCH is the leading online dating platform, with an estimated ~50% share of global dating users across its portfolio of brands, including Tinder and Hinge. The product portfolio consists of other general dating apps like OkCupid, Plenty of Fish, as well as apps with a certain focus such as BLK (for the Black community), Chappy (for the LGBTQ+ community) and OurTime (for singles over 50 years old).

It is an online dating company with both the biggest market cap and the largest user base.

How Does Match Group Make Money?

As mentioned, Tinder and Hinge are the current two flagship products contributing roughly 55% and 18% of the total revenue, respectively.

However, in terms of adjusted operating income, Tinder, as a more mature product with better economy of scale has a better margin: 49% vs 27% for hinge.

Almost all of the revenue comes from subscription fees and just around 2% is from in-app advertising.

Geography-wise, the situation is roughly like: Americas – 50%, Europe – 30%, APAC and the rest – 20%.

Industry and Competition

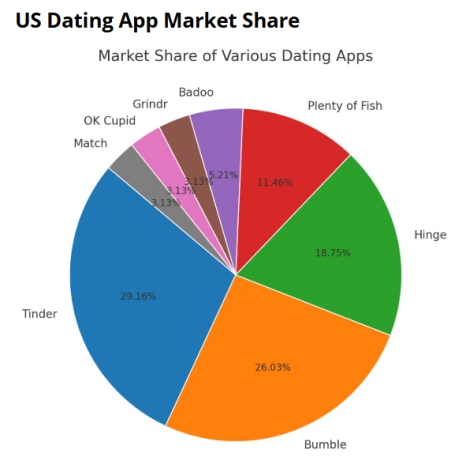

Dating app business is a crowded space, with no single dominant brand. However, Match Group owns 3 out of the top 4 dating apps in the US, so we can say that they dominate the market. However, Bumble is still quite a strong brand. Apart from that, we have Grinder which is the dominant app for the LGBTQ+ community, and several regional players (e.g. Coffee Meets Bagel in Asia).

Source: Developer Bazaar Technologies

However, we believe the main threat for MTCH does not come from inside but from outside the industry. Other social media platforms like Instagram, TikTok, Twitch, may not be dating apps per se, but they can serve the same purpose. Taking Instagram as an example, not only it emphasizes on visual content (photos) just like the dating apps but it has some significant advantages over them, such as 1) the user base is much larger; 2) Instagram can predispose towards a much more organic communication and 3) the social verification for Instagram is much easier (can judge by number of followers);

Growth Drivers

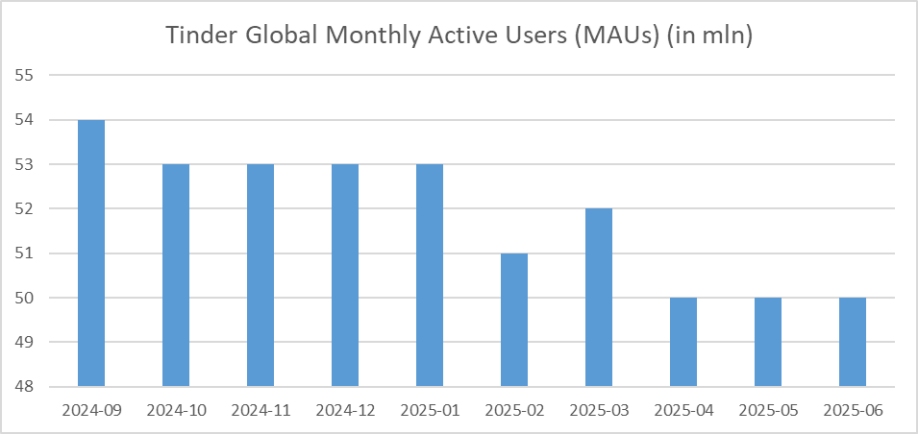

If we say Match Group (and Bumble) is in crisis, it won’t be an exaggeration. We can see for tinder there is an obvious downward trend in user decline:

Source: Sensor Tower

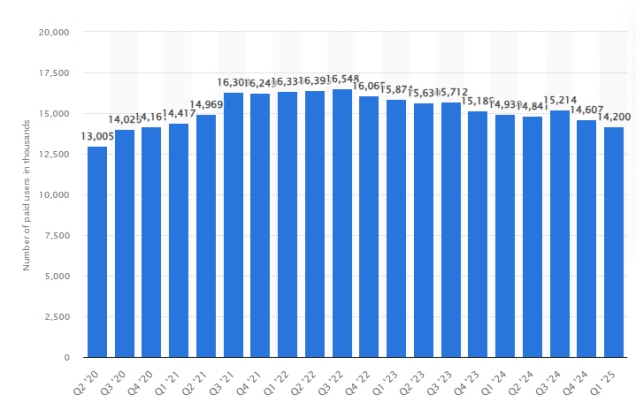

Also, the situation with paying users across all the Match Group platforms is not much different, with similar rate of decline.

Source: Statista

But, on other hand, there are certain positive aspects that can make Match Group a good turnaround story:

Reverse the user decline trend: Currently, investors are mostly focused on seeing a slowdown in the user decline, before any significant revenue and margin improvement… and that makes sense because users are the core of the whole business model – users bring more users and this brings revenue. In fact, we do see signs of bottoming out with MAUs in the last three months being flat at 50 mln.

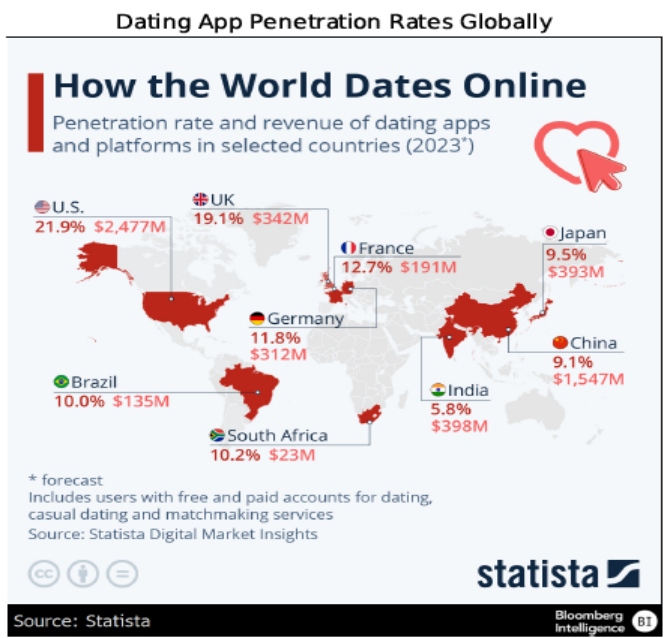

Hinge and the Global Penetration: A potential tailwind for MTCH is Hinge which is the only brand that is growing at 20%+ year-over year in terms of revenue. The app is already generating significantly higher revenue per user, and it is in early stage of expansion, as it is currently available in just a few countries, yet to see a wider expansion in Europe and Asia. Also, the margin for Hinge has a significantly lower margin but this is bound to change with the app gaining more traction. Dating apps are still not widely accepted in non-western countries but this may change as offline dating is becoming harder and harder.

Source: Company Reports

Source: Statista

Underspending on marketing: Match Group has recently undertaken employee lay-offs, and this can be seen as a step in the right direction to save more money and invest in marketing. Currently, the company underspends on marketing 17% vs Bumble which is 24%.

Network effect: The fact that Match has a bigger portfolio (more brands) under its belt vs Bumble, can be seen as a positive sign. In fact, dating app users often use more than one app at the same time and this increases the chance of a very new user starting to start using some of the Match Group’s apps.

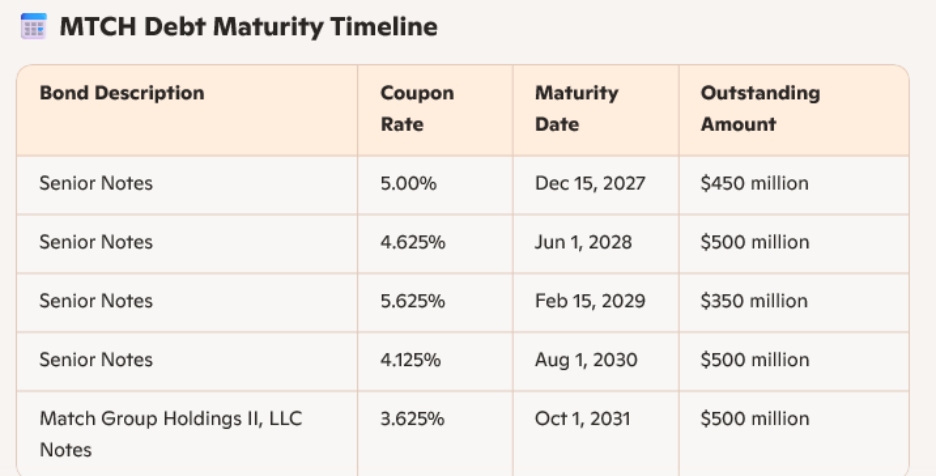

Debt situation is not as bad as others see it: Right now, the cash is just $0.4 billion vs with a total debt of almost $3.4 billion. However, the company is generating positive operating cash flows of around $900 billion, large enough to cover the interest expenses. Additionally, the majority of debt maturities are quite well distributed, and the next maturity is at the end of 2027.

Source: Company Reports

Valuation

According to our DCF estimate, the company is valued at around $35-40 per share. Valuation is very low at just 16x PE. This reflects the overall cautious stands related to the suppressed MAU numbers and the low barriers for competitors to enter. However, the growth potential with Hinge overseas is there.

Risks

Competition risk remains the biggest threat as the space is already crowded, and the people see non-dating app social platforms like Instagram as a viable alternative.

Recommended Articles