[IN-DEPTH ANALYSIS] Coupang: Dominating the South Korean Market One Step at a Time

Source: TradingView

Thesis

TradingKey - Coupang growth is fueled by the suitable macro environment in Korea, as well as the very strong business moat, namely logistics infrastructure. The impressive market share expansion (from 11% to 25% within five years) is probably the best evidence for it. The stable top-line growth rate and margin expansion are with a rather high level of certainty, which implies the stock price still has around 50% room for growth in the coming five years.

Company Overview

Coupang is the largest Korean e-commerce company, often referred as the “Amazon of South Korea”. However, this label is slightly inaccurate considering Amazon is primarily a marketplace (3P model) while Coupang is predominantly selling its own inventory (1P model), as nearly 80% of the revenue comes from products that are held by the company as inventory. Coupang is more like what JD.com is in China.

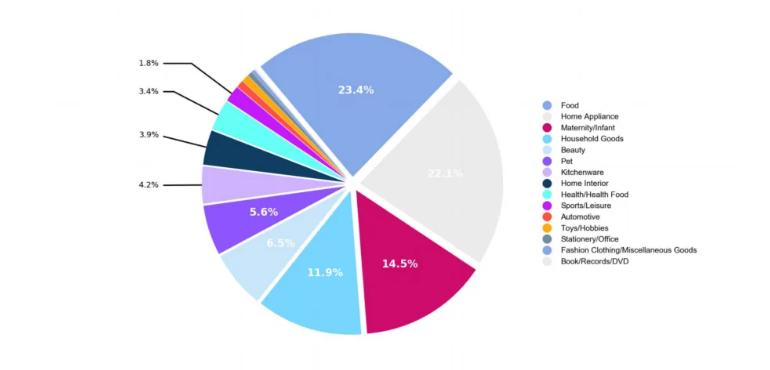

Currently, Coupang offers products spanning over a wide range of categories, including home goods and decor, apparel, beauty products, sport goods, electronics, and everyday consumables.

Source: TMO Group

70% of merchants are SMEs with less than $2.5 million of annual revenue. Most of these merchants do not have established sales channels, which makes them overly dependent on Coupang and distribution channels.

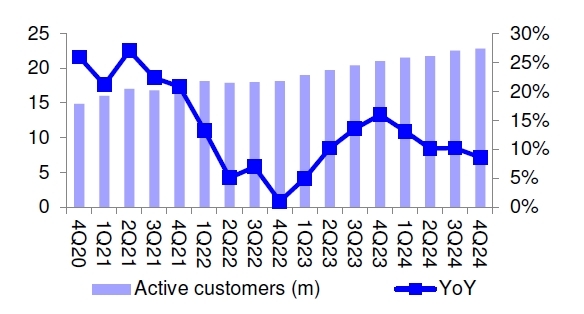

According to the most recent company data, 23.4 million users are using Coupang, which is 45% of the total country population.

Apart from the main 1P business, Coupang also has several other fast-growing business lines

- 3P marketplace

- Fulfillment Services for third party merchants

- Food delivery

- Taiwan operations

- Financial Services

- Membership revenue (Rocket WOW)

- Farfetch

The Key to Success

Source: ECDB

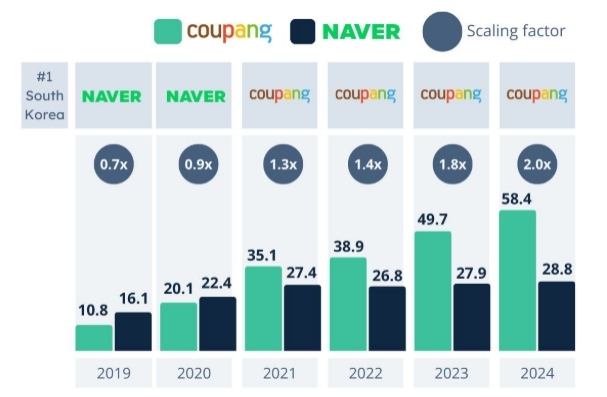

In 2021, Coupang took over Naver to become the largest e-commerce player in the country and now the company is confidently expanding its market share, which is around 25% at the moment. For reference, the market share in 2019 was just 11%.

The main reason behind the success is the very strong network of logistics and fulfillment centers that ensure wide coverage and timely delivery. The company is unmatched with the same day delivery of virtually all orders, something that neither domestic nor international players can achieve at this moment.

Interestingly, as they were founded in 2010, Coupang were 3P at first but gradually switched to 1P and started investing in their own logistics capabilities. Now with 100 fulfillment centers with a total of 4.7 million square meters, Coupang has easy access to the majority of the Korean population.

This also makes the return process smooth, just leave the goods at the door and they will be picked up and a refund will be initiated.

Industry Overview

Korea as an e-commerce market

Korea is one of the best countries to run an e-commerce business due to the following factors:

- Relatively small territory, not as spread out as the US and China

- Large population - approximately 51 million

- Very densely populated and predominantly urban – 80% of population in urban areas, 50% concentrated in Seoul Metro Area

- High purchasing power – average household income of nearly $4,000

- Digitally advanced consumers - 99.5% of households have internet access

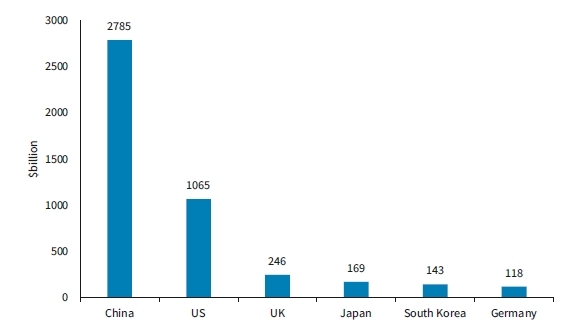

Unsurprisingly, Korea is the fifth largest e-commerce market just after China, USA, the UK and Japan. The country is also boasting one of the highest e-commerce penetrations globally with around 30%.

Source: eMarketer

Source: eMarketer

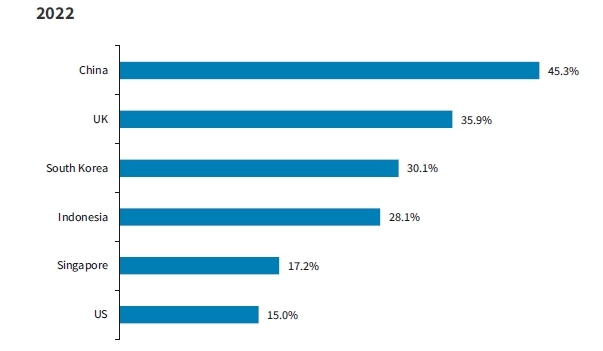

Despite the mature stage of the Korean e-commerce market, there is still a plenty of room for secular growth. The penetration of the local e-commerce market has all the chances to take over the UK or even China in terms of penetration, primarily due to the geographical and demographic characteristics.

Competition

Even though Coupang is a market leader, the Korean e-commerce market still can be considered as quite fragmented. This is different from America where we see Amazon being the undisputed leader or China where three players are taking up almost the entire market.

Apart from Coupang, other significant players are Naver, 11 Street and SSG. Naver is the equivalent of Alibaba but unlike BABA, Naver does not have a logistics arm, and they have to rely on third parties. 11 Street is backed by SK Telecom, while SSG is supported by Shinsegae, the most established chain of physical department stores.

However, Coupang is the only one with 1P model among the four, and the one with the most developed logistics and distribution network, ensuring fast delivery and product quality.

Other smaller scale local players are Lotte (another big retailer) and Kakao (the operator of the Korean version of WeChat).

The Korean market is also a target of large international players such as Amazon as well as all the three Chinese players, Alibaba, JD and Pinduoduo.

Despite the crowded space, Coupang has already developed its business moat by building their vast logistics network throughout the last decade. At this moment, it will be difficult for local players to replicate this network by themselves.

Even for the large foreign players it may not be an easy task to gain significant ground as they simply rely on cross-border commerce and the delivery takes much more than Coupang’s one day delivery.

Overall, in this crowded space, the mid-size e-commerce players will be the main losers of market share to Coupang’s logistics superiority and the international players’ ability to provide niche overseas goods.

Financials

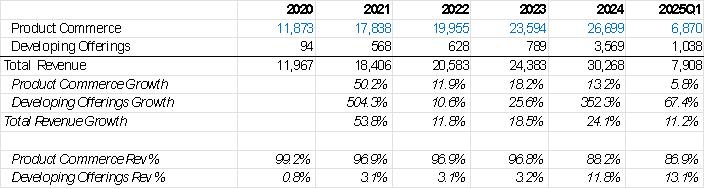

Coupang reports revenue in two segments:

- Product Commerce: 1P and 3P e-commerce, Rocket Fresh (grocery delivery), fulfillment services.

- Developing Offerings: Farfetch, Coupang Eats (food delivery), Coupang Play (online content), fintech, Taiwan operations

Source: TradingKey

*Farfetch is included in Developing Offerings as of January 30th, 2024 - $1.7 billion

*Revenue growth for Product Commerce in 2024 and 2025Q1 is 18% and 16% based on constant currency

The growth in Product Commerce is driven by both an increase in active users and increased user spending.

Source: Company Data, Deutsche Bank

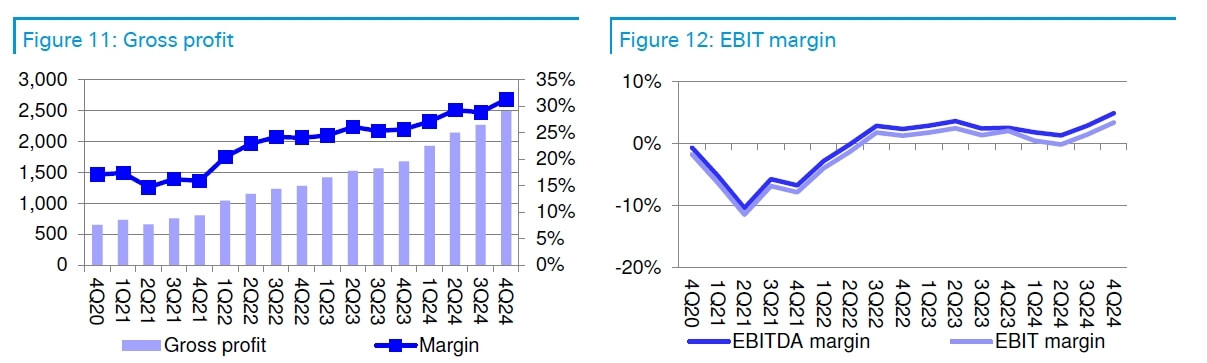

Profitability also expands healthily with the introduction of high margin business such as 3P e-commerce and fulfillment.

Source: Company Data, Deutsche Bank

The balance sheet of Coupang has two very strong aspects. Firstly, the cash is significantly larger than the debt, where the interest income on the cash offsets the interest payments on the debt.

Secondly, throughout the years, the company maintains a huge amount of accounts payable, much more than the accounts receivable and inventories combined. This means Coupang is operating on a negative working capital. Negative working capital for e-commerce and retail is a positive sign as the company collects money from customers very quickly and delays payment to suppliers, creating a surplus of working capital cash that can be used for financing the daily business operations.

Source: Company Filings, TradingKey

Source: Company Filings, TradingKey

Potential outside commerce

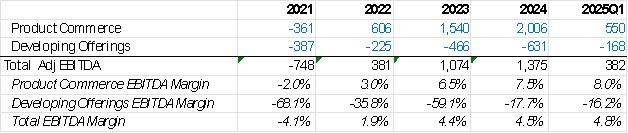

The non-commerce businesses still constitute a rather small fraction of the total revenue of just below 15%. However, they are seen as important drivers for the future. Also, the EBITDA margin loss has been constantly shrinking.

Source: Company Filings, TradingKey

Here is a brief overview of three business lines that, despite their nascent stage, are going to be observed by investors:

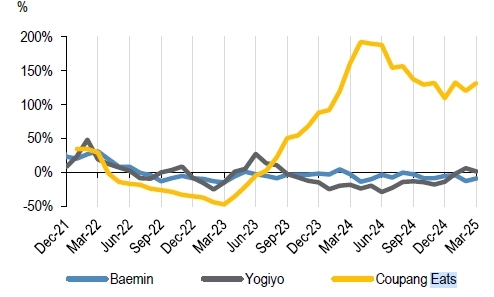

Food delivery

The food delivery market in Korea is dominated by three players: Baemin (70%), Yogiyo (20%) and Coupang Eats (10%). Coupang as the youngest player entered the market in 2019 and it already controls 10%. Coupang is particularly strong in Seoul. Coupang is close to breakeven here.

Source: wiseapp

Taiwan

Taiwan shares a lot of similarities with Korea when it comes to geography and demographic characteristics. Currently, the e-commerce landscape is dominated by Sea’s Shopee (Singapore) and local players like Momo. We don’t see presence of Amazon or the big Chinese players. Coupang will follow the same procedure as in Korea, as they gradually expand its logistics footprint.

Farfetch

Coupang officially completed the acquisition of Farfetch in January 2024. Farfetch is one of the most renowned online marketplaces for luxury goods. However, the company was constantly struggling in the past due to questionable business decisions. Coupang is currently trying to turn around the business.

Assumptions and Valuation

The current reported PE ratio of Coupang is over 200x but this number does not have much meaning. We would like to estimate the profit five years later when the operations are more mature.

Currently the total revenue growth is around 20% on a constant currency base but we expect the top line to grow in low teens in the coming five years. We do expect core commerce to grow around 10% - not as much as recent years but also still above the broad Korean e-commerce market. For the other fast growing business lines like Eats, Taiwan and Farfetch, the growth can be much faster at around 20% as these ventures are still in early stage. Thus, the expected revenue in 2029 might be in the range of $50-51 billion.

In terms of profitability, the operating margin should be around 7-8%. While we acknowledge the increased role of high margin businesses like 3P commerce, fulfillment and food delivery, we do not expect a huge ramp up in profitability as it takes a while for these businesses to be profitable on operational level.

With these assumptions the company is currently trading at 20x the expected earnings for 2029. This is low if we compare it to a direct US peer like Walmart, which is currently traded at 40x. However, as a Korean company, there should be a Korean discount, and we believe 30x for Coupang is reasonable. This implies 50% upside potential or a target price of $40-45 USD per share or an expected share price growth of around 10% per year for the coming five years.

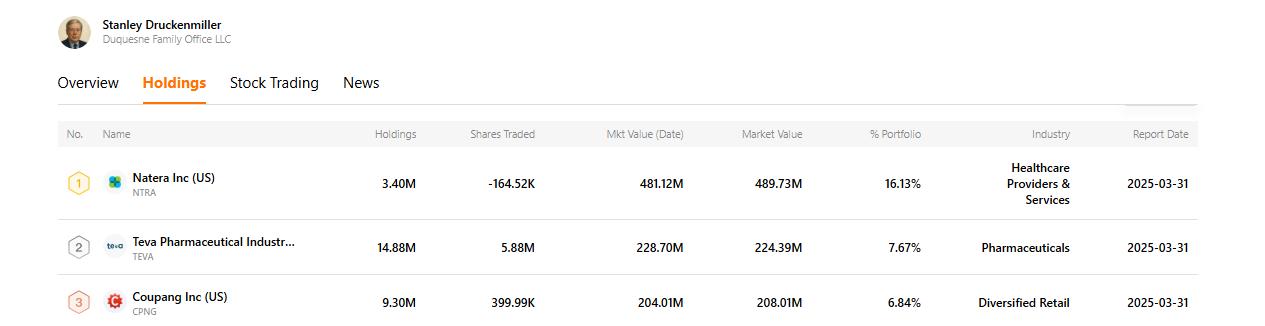

The Druckenmiller Factor

Source: TradingKey

Coupang is the third largest holding of Stanley Druckenmiller’s Duquesne Capital, as he recently increased its holdings in the company.

Druckenmiller’s investing approach is often associated with top-down investing – bets on macro trends. Coupang fits this profile as the company benefits from the socioeconomic and demographic structure of South Korea, as this is what fuels Coupang’s remarkable growth.

Learn more about Druckenmiller’s and other star investors’ bets at TradingKey’s Star Investors.

Risks

Competition remains the biggest risk, as the Korean market still has a lot of e-commerce players. Intensified competition in the field would mean a slowdown in profitability and revenue.

Another potential risk is any kind of strategic missteps into the new business ventures (Farfetch, Taiwan) that could lead to widening operating loss or destruction of capex.

Recommended Articles