Lululemon’s Valuation Reset: Why Market Sentiment Diverges from Fundamentals

- Q1 FY2025 revenue grew 7% to $2.37 billion, with international sales rising 19% and Americas up 3%.

- Gross margin expanded 60 basis points to 58.3%, while operating margin declined 110 basis points to 18.5%.

- Inventory increased 23% YoY to $1.7 billion, raising concerns about demand forecasting and potential future margin pressure.

- Forward P/E compressed to ~20x, down ~51% from the five-year average, despite stable fundamentals and global expansion potential.

Lululemon (LULU) has been almost synonymous with category-defining athletic apparel that carries both cultural prestige and premium valuation multiples. But after Q1 FY2025 results, a jarring 22% after-hours drop suggests Wall Street is beginning to doubt if the brand's growth engine is losing steam.

Even after beating top-line expectations and projecting EPS expansion in FY2025, valuation compression is gaining speed. At a forward P/E of almost 20, half the five-year average, the market is reflecting waning confidence in Lululemon's long-term moat while fundamentals remain bolstered. This paradox, in which high-margin, cash-generative businesses get derated by investors, implies a profound reset is occurring, not simply in sentiment but in investor expectations.

Lululemon is no longer a story of spectacular growth. It's a story of margin durability, inventory control, and international execution. Lululemon now has to demonstrate that it can deliver operating leverage in a decelerating-growth period while defending premium brand value. What's playing out isn't a collapse but a repricing. And for investors, it raises a crucial question: did the pendulum get too far?

A Brand in Transition: Long-Lasting Model, But Paced Slower

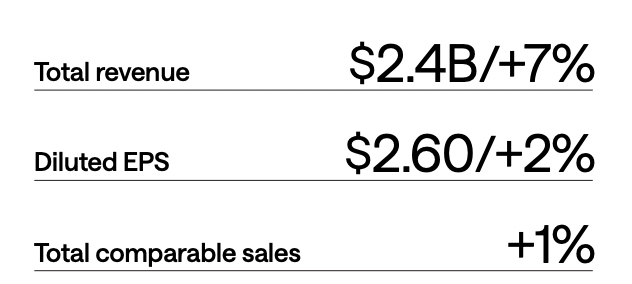

Lululemon's Q1 FY2025 results presented a company in transition, still structurally sound, but obviously slowing down. Total revenues climbed 7% YoY to $2.37 billion, or 8% constant currency.

Source: Lululemon Quarterly Infographic

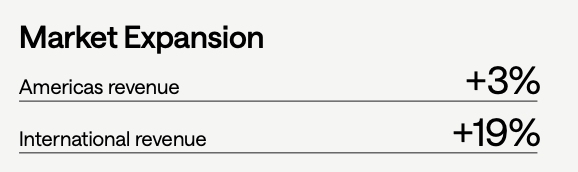

International sales were the driver, ramping 19% (20% constant currency), while Americas revenues rose only 3%. Importantly, comparable sales rose only 1%, with Americas comps declining 2%.

Source: Lululemon Quarterly Infographic

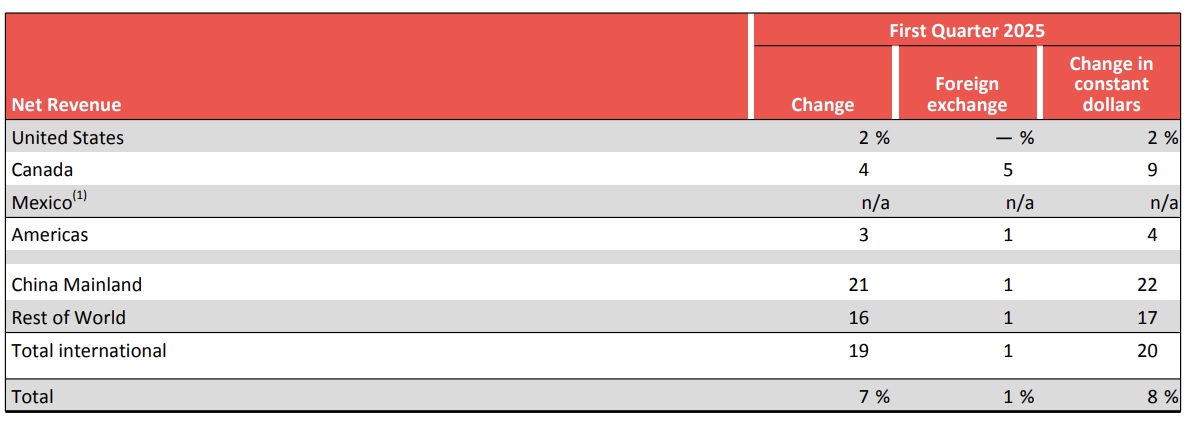

Source: Lululemon Quarterly Financial Supplements

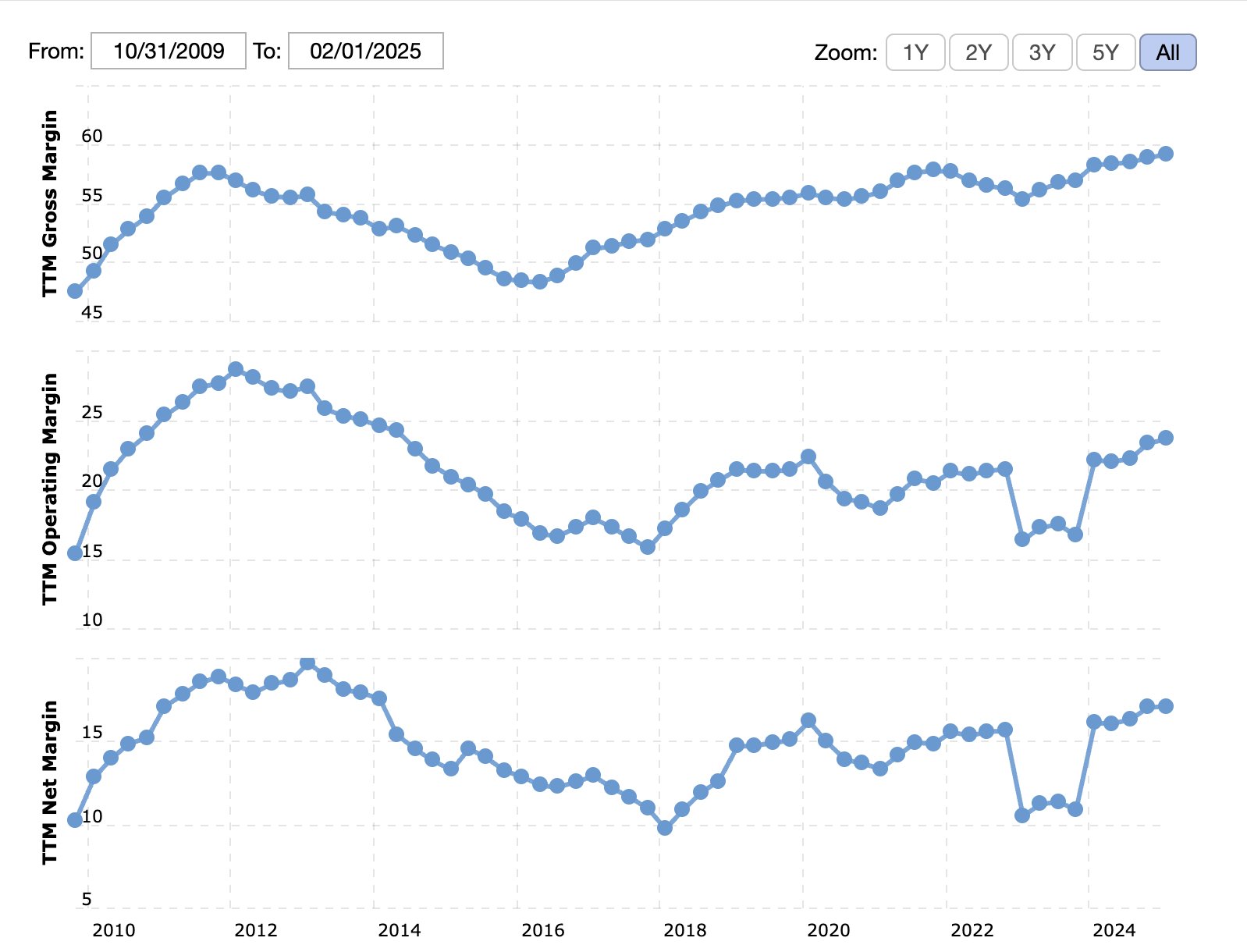

This divergence speaks to the initial manifestations of saturation in Lululemon's underlying U.S. market, a segment that contributes over 60% towards its entire revenue base. In the face of macroeconomic headwinds, the company kept gross margin constant, widening it 60 basis points to 58.3% due to full-priced selling and controlled discounting.

Source: Margintrends, Lululemon Profit Margin 2010-2025

Nonetheless, operating margin decreased 110 basis points to 18.5% due to SG&A inflation and the deleveraging of fixed costs. Net income of $314.6 million (+2% YoY) and diluted EPS of $2.60 are an indication of stability, rather than dynamism. The company also repurchased $430 million of shares, indicating faith in its valuation but also pointing to scarce opportunities to reinvest.

Inventory rose 23% YoY to $1.7 billion, well ahead of top-line progress and sounding the alarm on demand forecasting. Unit expansion of 16% reflected an uptick in the mix to premium-priced SKUs or delayed clearance. Though management is optimistic, with Q2 revenue guidance of $2.535–$2.560 billion (+7–8%) and FY25 EPS in a range of $14.58–$14.78, investors are becoming less sure that Lululemon can return to its previous trajectory without taking on risk in terms of margin.

Source: Macrotrends, Lululemon Inventory 2010-2025

Market Position vs. Competitive Pressures: A Narrowing Lane

Lululemon's brand moat is still powerful when it comes to loyalty, innovation, and marketing based on communities, but the world outside is transforming quickly. Nike, Alo Yoga, and Vuori are pushing hard in the athleisure segment, each jockeying for mindshare amongst Gen Z through direct-to-consumer models, influencer networks, and quicker fashion cycles.

While Lululemon's past is founded on well-made, purpose-built equipment, that advantage is fading as technical capabilities become commodified. Priced at a premium, Lululemon still commands it, but macro uncertainty and consumer discretionary fatigue are building, putting this price power under latent stress. Vuori is already discounting prices while replicating the look.

Lululemon's move into men's and footwear, central to diversifying its top line, remains to be fully verified in terms of margin accretiveness. Early traction is seen, but success is never easy or guaranteed in commodity-dominated categories with established players.

Globally, Lululemon is underpenetrated, providing a long-term leverage point. China experienced Q1 revenue expansion of 21% (22% in constant currency), reinforcing global brand relevance. However, geopolitics, localization demands, and brand adaptation based on culture are challenges that are less evident in its domestic market. In addition, elevated international square footage has not yet translated into material operating leverage, inducing a delay in investment versus margin accretion.

Valuation Contraction: A Structural Repricing, or an Overreaction

Valuation is where Lululemon's story comes under most scrutiny. Its forward P/E of ~16.3x (Non-GAAP), close to the sector median (~16.6x), is a staggering ~60% discount to its own five-year average of 41x. On other metrics, compression is even more dramatic: EV/EBITDA FWD at 10x is down ~65% from its five-year average, while Price/Sales FWD at 2.6x is down ~54%.

These levels suggest the market now considers Lululemon a mature, slower-growth discretionary brand and not a structurally advantaged compounder. Even the PEG ratio, normalized to account for growth, is a modest 0.89. Still, the company's 6.7x Price/Book is still rich compared to the industry (2x), indicating it is still being valued as a premium asset, merely with subdued assumptions about growth.

The disconnect between rich discounted cash flow-based valuation and still-rich book value implies consternation in the market: Is Lululemon still a growth story or becoming a quality value play? Most importantly, EV/Sales TTM is at 2.7x, 117%+ over sector median, even if top-line expansion slowed and inventories ballooned. Such an imbalance is a signal of a valuation floor emerging, not from bullish buyers, but from normalized sector comparables.

Threats: Margin Slippage, Inventory Builds Up, and a Brand in Midlife

The most apparent risk to Lululemon's thesis is margin erosion fueled by high SG&A and decelerating fixed cost absorption. As operating margin declines 110 bps and SG&A gets closer to 40% of sales, the journey to EPS expansion rests increasingly on cost discipline rather than top-line ramp. A mistake in discount or marketing spend will exacerbate deleverage.

Another warning signal is inventory expansion outgrowing sales. A 23% YoY increase in inventory, contrasted with a 7% sales increase and merely 1% comp sales expansion, is either a preholiday cycle build or an overestimation of demand elasticity. If promotional sales ramp up to liquidate excess inventory, margin expansion may rapidly reverse.

Brand fatigue is a less obvious but actual problem. While Gen Z shoppers go in on quicker trends and lower-cost substitutes, Lululemon is forced to reinvent product lines without losing its identity. Brand heat in past cycles might not be enough to support 30%+ valuation appreciations unless fiscal execution comes back into sync with the inspirational brand story.

Conclusion: A Quality Brand Entering a New Phase

Lululemon is still a high-caliber company with desirable brand value and fiscal restraint. Yet, its investment thesis is transitioning from high-growth apparel disruptor to global premium lifestyle platform with normalized returns and diminished comps.

As forward multiples are already halved but fundamentals are still relatively intact, the market might already have priced in too much pessimism. Long-term investors get a re-entry point here if Lululemon can restore comp reacceleration and get in control of inventory. But the bar is elevated now.

Lululemon will now need to demonstrate that it can prosper in the absence of exponential U.S. expansion. Upside is still there, but it requires execution, not storytelling.

Copyleaks Report: https://app.copyleaks.com/report/0c4jtl8fgfeh3u1e/preview?key=44dbgft2avnrutxa&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

Recommended Articles