Uber’s Quiet Transformation Pays Off

- $2.3 billion Free Cash Flow in Q1 2025, with GAAP net income of $1.78 billion and 10%+ operating margins, marking a financial inflection point.

- Uber One loyalty flywheel drives 3.4x higher spend per user and lower CAC, enhancing monetization across Mobility and Delivery.

- AI-powered platform economics enable real-time pricing, supply optimization, and ad monetization, boosting margins and reducing incentives.

- Delivery margins rival top peers, with Uber Eats Ads adding high-margin revenue and backend shared with Mobility segment.

- Global diversification mitigates risks, with all regions growing and a $6 billion cash buffer limiting refinancing exposure.

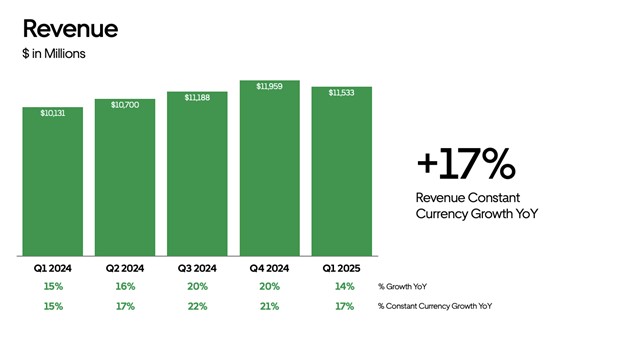

TradingKey - For decades, Uber (UBER) has been unfairly stereotyped as a growth-at-all-costs, volatile, unprofitable gig platform that is always reliant on growth, incentives, and subsidies. That narrative is now fundamentally shattered. As of Q1 2025, Uber has quietly navigated across a financial Rubicon, becoming one of the most capital-efficient scaled platforms in the consumer technology space. During the quarter, the company generated $2.3 billion in free cash flow and $1.9 billion in adjusted EBITDA on $11.5 billion in revenues, 35% year-over-year EBITDA growth. But the market has been sluggish to internalize this shift, holding on to outdated models that are no longer applicable to Uber’s platform economics.

Source: Uber Technologies, Inc. Q1 2025 Earnings

The myth that Uber is a margin-bleeder business model is based on historical losses and battles at the regulators' level. But the truth now is that the company is a precision-engineered operating machine with positive GAAP net income of $1.78 billion, GAAP operating margins of more than 10%, and a way to drive compounding earnings per share. Significantly, the company has resolved to return capital, having already spent $1.8 billion on share repurchases this quarter alone, shrinking the share count and restructuring per-share metrics.

Uber's transition is not a cyclical narrative. It is a tale of strategic progression, from subsidized scale to monetized engagement. And at the core of this shift is a less appreciated engine: a data-intensive, many-sided logistics platform that can create recurring, high-margin cash flows across several verticals. Uber stock has only just been re-rated. The wider market is still holding onto ride-hailing companies like Lyft or asset-intensive players like FedEx, failing to appreciate the hybrid form of Uber's new economics: asset-light, AI-native, platform-leveraged, and free cash flow generative.

Rides to Revenues: Uber's business model reinvented

Uber now has three core segments, Mobility, Delivery, and Freight, powered by a common global infrastructure. Each of these verticals is greater than a stream of revenue; they are interconnected systems crafted to drive the most usage, monetization, and customer lifetime value at the lowest possible incremental price.

Source: GrandViewResarch, Global Ride Hailing Services Market

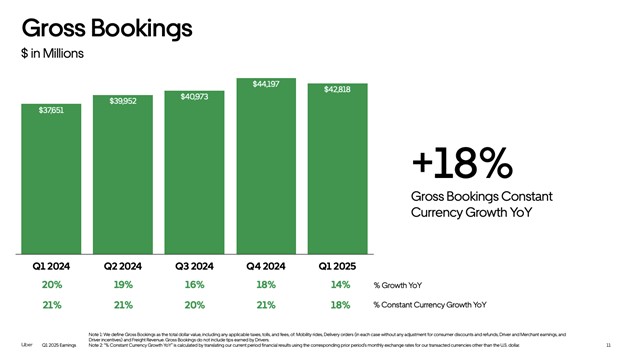

Mobility is Uber’s foundation, with $21.2 billion in gross bookings in Q1 2025 and $6.5 billion in revenue, 15% YoY growth. Segment Adjusted EBITDA reached $1.75 billion, up 19%, demonstrating evident operating leverage. Consumer trips grew 18% YoY, but Monthly Active Platform Consumers grew just 14%, with rising frequency leading to greater per-user revenue. Far from assumptions regarding commoditization, Uber’s pricing power remains: average revenue per trip continues to scale even with the headwinds of regulation and localized promotions.

Source: Uber Technologies, Inc. Q1 2025 Earnings

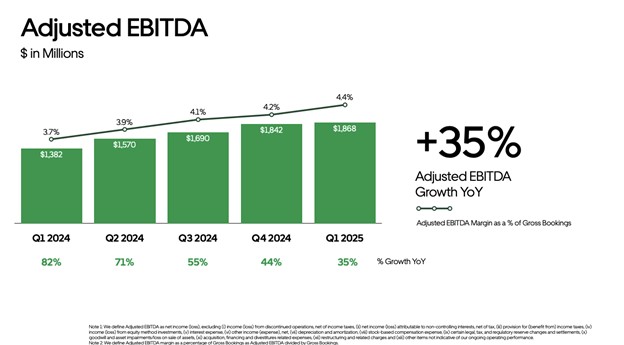

Delivery is Uber’s next big profitability driver. The business made $3.78 billion of revenue and $763 million of Adjusted EBITDA, a 45% YoY growth. Gross bookings hit $20.4 billion, up 18% on a constant currency basis. This is no longer a burn-intensive, low-margin business. Uber’s common backend for Mobility and Delivery, with shared customer databases, fulfillment algorithms, and real-time ETAs, delivers margin economics that stand-alone players like DoorDash cannot. The inclusion of Uber Eats Ads is a continuing sleeper success, generating incremental revenue with essentially a 100% margin bump.

Freight, the weakest of the segments, stabilized. Revenues dipped 2% to $1.26 billion, but Adjusted EBITDA loss reduced to $7 million from $21 million. That the decline in losses is narrowing in a soft freight cycle reflects cost management discipline and portends potential profitability on the way back up for volumes. Uber’s logistics layer native to the platform provides long-term optionality to tap in to enterprise shipping networks.

Source: Uber Technologies, Inc. Q1 2025 Earnings

Uniting these segments is Uber’s orchestration layer, its AI-powered dispatch, dynamic pricing in real time, and trip-routing infrastructure, that offers operational scale without matching cost. A critical aspect is that these segments aren't siloed. Uber One membership subscribers, its bundled membership, are more likely to use both Mobility and Delivery services, representing more than 3.4x the spend of non-members.

The Unseen Operating Flywheel: Pricing Power, Platform Synergies, and AI

Uber’s strongest engine is neither its fleet nor its footprint; its is the behavioral loop of feedback that is ingrained throughout the platform. Each trip, order, and click creates data that is fed back to influence pricing, matching, and ETAs. And this data fuels an AI-driven model for operation that minimizes costs, maximizes supply, and enhances user retention.

Uber One membership is at the center of this flywheel. The program has tens of millions of members now, who enjoy perks such as cheaper fees, priority support, and special deals on both rides and deliveries. These customers are more loyal, consume more services, and are less likely to churn. Uber is, in turn, able to spend less on acquisition, tighten the CAC, and grow ARPU. For a company that was once mocked for cash-burning customer incentives, Uber has created a self-sustaining monetization model.

In addition, Uber’s AI-powered dispatch systems drive greater asset utilization among its driver fleet. The system adjusts supply in high-demand areas in real time and forecasts latent demand according to weather, events, and past patterns. This not only minimizes rider wait times but also maximizes driver earnings per hour, increasing retention while decreasing Uber’s incentive costs.

On the merchant side, Uber Eats Ads has quietly become a high-margin powerhouse. Merchants now pay for visibility in the app, turning ad dollars into direct transaction volumes. Since Uber owns the demand layer already, it monetizes attention natively, something that both Amazon and Instacart have done to retail, but few have done to food delivery.

Source: Company Data, Bloomberg, Daxue Consulting, The Information

AI is also seeping into cost structure optimization. Uber applies predictive modeling to forecast fraud, insure against provisioning, even to negotiate with municipalities based upon simulation-driven urban impact projection. These optimizations, lurking behind the scenes, drive margin resilience, properly an invisible area to the casual observer but essentially the key to deciphering Uber’s long-run profitability path.

Valuation Reboot: Under the Surface of Uber’s Multiple Expansion

Uber’s valuation is optically high in some GAAP metrics but materially undervalued when normalized, sector-adjusted metrics are considered. While the firm’s GAAP P/E (TTM) is 16.2x, a number that may give value investors reason to hesitate, this figure obscures Uber’s structural leverage and free cash flow heft. On a Non-GAAP TTM basis, Uber is only trading at 13.41x earnings, a 33% discount to the sector median of 19.3x. This spread is a function of Uber’s special combination of operating leverage and items like stock-compensation charges and regulatory fees that skew the HCP/e ratio.

Looking ahead, Uber’s forward P/E (Non-GAAP) of 25.4x remains at a premium to the sector median at 19.3x, but this is warranted in light of Uber’s faster growth pace, multi-vertical cash conversion, and buyback tailwind. By contrast, the forward PEG ratio of 0.87x is nearly 50% below the sector, which is a classic indication of GARP stocks that imply substantial earnings growth against the price paid.

From an EV/EBITDA perspective, Uber’s 42.1x TTM EV/EBITDA and 22.4x FWD are high relative to peers, but this is due to backward-looking EBITDA bases. Uber’s Q1 YoY EBITDA grew 35%, and the momentum is strong going forward. Crucially, these multiples collapse quickly upon including Uber’s $8 billion+ 2025 EBITDA guidance, getting EV/EBITDA to around 13–15x on a normalized basis, in line with large-scale software platforms.

The most underrated metric is Uber’s Price-to-Cash Flow. Though its P/CF (TTM) of 25.5x currently may represent only a slight premium over the sector median of 15.32x, it grossly undervalues the acceleration at Uber. Uber produced $2.3 billion of free cash flow in Q1 alone, representing a run-rate of $9 billion, or a forward FCF multiple of closer to 10.1x. Factoring in ~$6 billion of net cash, Uber’s FCF yield is over 4.5%, an elite level among Industrials and Tech-adjacent peers.

Even within more conventional valuation models, Uber's 3.8x FWD Price/Sales stands below high growth software or logistics platform peers even with higher margins and user engagement dynamics. With a 7.4x FWD Price/Book, Uber is trading above traditional transportation companies but is in reasonable confines considering its capital-light design, asset productivity, and platform flexibility.

Source: Precedence Research

Together, Uber's valuation picture is a textbook mispricing of growth tenor and margin expandability. The market persists in pitting Uber against linear operators such as FedEx or commodity platforms like Lyft, dismissing the AI-driven flywheel effects, cross-polination of networks, and high-margin ad monetization. With earnings now compounding, share count decreasing through buy-backs, and structural FCF transparency, Uber is now behaving like a misperceived compounder rather than a late-stage growth stock.

Risk, Regulation, and the Global Cash Machine

While the path that Uber is on is encouraging, there is some risk. The most material is regulatory, centered on worker classification and tax. The UK HMRC is currently challenging Uber’s VAT treatment under the Tour Operators Margin Scheme, leading to a $1.8 billion provisional tax assessment. Although Uber has prepaid and appealed, keeping this away from its P&L, the possibility exists that this could have a material effect on cash flows or necessitate structural changes in the UK.

Secondly, macro sensitivity is an influence. A pullback or slowdown in consumers' willingness to spend could temper volumes, particularly in discretionary segments of travel. But Uber’s geographic diversification across North America, EMEA, LATAM, and APAC protects against single-region shocks. All regions grew in Q1, with EMEA increasing 20.5% YoY and APAC increasing 7%. On the balance sheet, Uber is strong. Uber carried $6.0 billion in unrestricted cash at the close of Q1 with no revolver drawdown. Leverage is moderate compared to EBITDA, and Uber has no imminent refinancing risk.

Conclusion

Unlike most post-pandemic technology darlings, Uber is not reliant on the capital markets to finance growth or return capital to shareholders. Uber is no longer a growth bet on speculation. It is now a cash flow-producing, AI-empowered, capital-light platform with global scale and layered monetization. Investors are re-casting their opinion on Uber based on the sustainability of FCF generation and shareholder yield. Its valuation today, even so, underestimates the potential. It is a logistics platform, a utility for the consumer, a cash flow machine, cloaked as a past ride-hailing business. Its next chapter is not survival. It is compounding.

Recommended Articles