The Shift Inside AMD No One Sees

- AMD’s Q1 2025 revenue hit $7.4B with 36% YoY growth, driven by EPYC CPUs and MI300 GPUs.

- The ZT Systems acquisition enables rack-scale integration, expanding AMD’s addressable market and lifting Data Center margins to 25%.

- ROCm 6.4 and AI container updates deepen developer stickiness, positioning AMD as a CUDA alternative with open-source appeal.

- With a 2.5% FCF yield and PEG ratio of 0.87, AMD remains undervalued relative to AI growth and peers.

Tradingkey - The general story in the case of AMD (AMD) today is one of decent growth, careful optimism, and competitive catch-up. That's short-sighted. Behind the beat on top-line earnings and cyclical bounce in the PC and gaming verticals, AMD is experiencing a deeper structural transformation with significant consequences. The $7.4 billion Q1 2025 revenue beat and 36% YoY growth merely suggests as much.

The actual thesis is in the intersection of rack-scale AI infrastructure, re-architected software ecosystem (ROCm), and the ZT Systems acquisition, as it makes AMD a full-stack challenger in the $500 billion AI accelerator TAM. The thesis of the article is that AMD is not just a second-string chipmaker in the shadow of Nvidia but a misunderstood platform company at an inflection point. The current valuation multiples of the market for 29x forward P/E, 2.5% FCF yield and PEG under 0.9 do not factor in AMD's embedded operating leverage, under-valued data center business, and systems-level differentiation.

.png)

Source: IoT Analytics

The Full-Stack Ascent: From Component Supplier to Platform Orchestrator

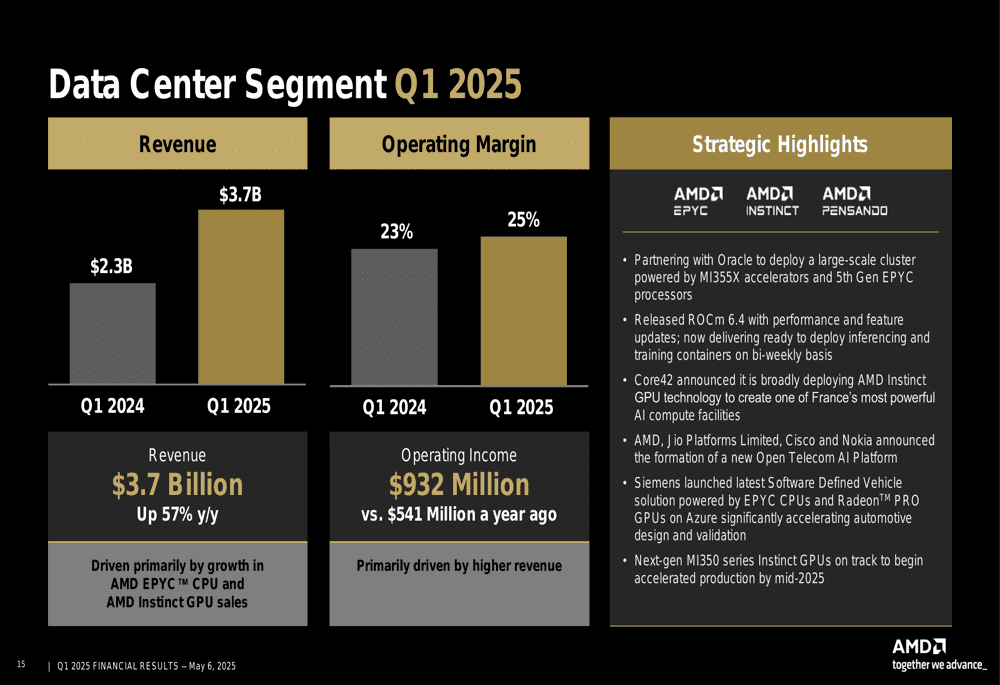

AMD's Q1 numbers shed light on its changing persona. Data Center revenue grew 57% YoY to $3.7 billion on the strength of EPYC CPU and MI300 Instinct GPU. But the important shift isn't in unit quantity, it's in integration. The completion of the ZT Systems merge on March 31, 2025 gave AMD end-to-end design competence for rack-scale systems, in effect bringing itself from silicon vendor to systems integrator.

That opens AMD's addressable market and margin profile exponentially. Rack-level design implies higher ASPs, improved power/performance optimization, and closer customer lock-in, typically the domain of Nvidia or vertically integrated hyperscalers.

Source: AMD’s First Quarter 2025 Financial Results

In the meantime, AMD is using ROCm 6.4 and AI software container deployments to enhance stickiness. Inference and training container bi-weekly updates mark the shift towards developer-driven platform economics rather than hardware share. Collaborations with Oracle, Core42, and Siemens support cross-industry affirmation. AI software integration with MI300-class GPUs replicates Nvidia's CUDA moat in open-source guise. The ramped-up Ryzen AI PC product line powered by Ryzen AI Max+ and 300 series processors supports the architecture by sowing an edge-to-cloud AI continuum, a play aimed at enabling end-to-end data observability and compute utility.

The Competitive Landscape: Catching Nvidia with Infrastructure-Led Playbooks

Nvidia leads the story and market capitalization, yet AMD's go-to-market differentiation deserves closer examination. Nvidia has a software moat through CUDA and deep hyperscaler pipelines while AMD is strategically outflanking in a systems play. How the addition of ZT Systems enables it to do rack-level customized deployments tailored to customers' workloads is something Nvidia, which frequently outsources integration, can't effectively match.

In addition, AMD's alliances are not public relations vanity. Oracle's implementation of MI355X accelerators in hyperscale environments and Core42's AI deployment in the flagship AI facility for France are real-world indicators of demand elasticity for something other than Nvidia. At the same time, the Open Telecom AI Platform with Jio, Cisco, and Nokia is an example of horizontal alliance strategy as opposed to vertical integration such that the company can scale without controlling every node in the stack. Conversely, Intel is stuck in delays and uneven execution, and Arm-based AI chip vendors do not have the software maturity or ecosystem depth that AMD currently has.

On an in-per-watt and in-per-TFLOP basis, critically, AMD is pricing aggressively. And with ROCm's increasing compatibility with top frontier models such as Meta's Llama 4 and Google's Gemma 3, the difference between Nvidia's premium pricing and AMD's value play becomes a material competitive factor.

Strategic & Financial Deep Dive: Where AI Meets Margin Expansion

The company's $0.96 Q1 2025 non-GAAP diluted earnings per share was 55% higher year-over-year on $1.6 billion of net income. Gross margin widened to 54% non-GAAP from 52% in the previous year on richer Ryzen processor mix and strong EPYC pull-through.

.png)

Source: AMD’s First Quarter 2025 Financial Results

The company's free cash flow jumped to $727 million representing a 10% FCF margin amidst high CapEx ($212M) related to integration as well as ramping MI300 production. The Data Center segment by itself generated $932 million of operating income on $3.7 billion of sales, representing a 25% margin.

.jpg)

Source: Finbold

The client segment was typically cyclical but produced a surprise 109% YoY growth in operating income on the back of adoption of 16-core Ryzen 9950X3D processors and notebook refresh cycles. Gaming revenue declined YoY on the back of semi-custom softness but remained flat sequentially, suggesting potential troughing.

AMD's OpEx leverage is also strengthening. Even after swallowing up ZT Systems, non-GAAP OpEx only grew 5% QoQ as R&D intensity continues at ~$1.7B, an indication of AMD investing all through the cycle. Of particular note was adjusted EBITDA of $1.95 billion, 50% margin versus $1.295 billion last year, reflecting platform convergence scale benefits.

On the balance sheet at the end of Q1, AMD had $7.3 billion in short-term investments and cash on hand, up 42% from the previous quarter, financed in part by $950 million commercial paper and $1.5 billion of new debt to finance the ZT transaction. Debt was at $4.16B but still low compared to equity ($58B) and the FCF path.

Valuation Recalibrated: Pricing Power Meets Market Skepticism

With a trailing non-GAAP diluted EPS of $0.96 during Q1 2025, AMD's run-rate on an annualized basis implies forward non-GAAP diluted EPS of approximately $3.84. Applying this to AMD's trading range of ~$111/share currently, the stock has a price to earnings ratio of ~29x forward non-GAAP earnings. The multiple tightens upon adjusting for AMD's Q1 gross margin increase, extended operating leverage, and potential gross margin normalization back to 56–58% following the one-time $800M export surcharge in Q2.

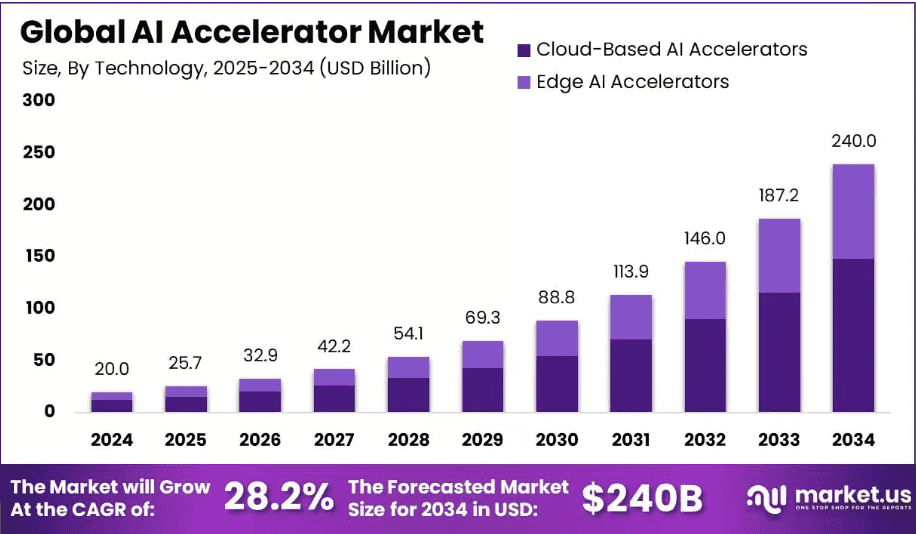

Consensus analysts project AMD's target price at $197.85 in 12 months, representing ~78% upside from here, and put AMD's PEG ratio at 0.87, significantly lower than Nvidia's >1.7 and the ~1.2 peer-group average. That divergence highlights potential mispricing. Although Nvidia is trading on 36x forward earnings with higher growth, AMD's valuation factors in substantial doubt on it being able to drive MI300X take-up and capture the $500B AI accelerator TAM it now has in its sights with integration of ZT Systems.

Source: market.us

Free cash flows also underpin the rerating case. AMD produced $727 million of Q1 FCF (+92% YoY), which translates into an implied ~$2.8 billion FCF annualized, or 2.5% FCF yield. Adjusted for the one-time reserve charge on inventory in Q2, AMD's normalized FCF yield would be close to 3.2%, which positions it favorably relative to large-cap tech comps at comparable stages of growth.

Risks: Supply Chains, Export Controls, and Execution Timelines

Although the structural thesis stands, AMD has material near-term concerns. The $800M write-off in inventory in Q2, attributed to U.S. export controls for high-end GPUs, is indicative of regulatory vulnerability in AI supply chains. Although management assures these are one-time charges, their effect on quarterly performance and sentiment can be a negative drag on multiple expansion. Second, integration of ZT Systems is in its early innings. Divestiture of manufacturing is in progress, though slippage in realizing rack-level synergies or margin gains has the potential to reset expectations.

Moreover, AMD's ROCm ecosystem, although maturing, lingers behind CUDA in terms of community usage, and software compatibility gaps may slow onboarding for risk-averse enterprise customers. In conclusion, there are also wider macro risks at play. A deceleration in hyperscaler CapEx or wider technology multiple compression on the back of rates or geopolitics would put pressure on valuation despite strong fundamentals. Therefore, the bull case is still dependent on timely execution.

Conclusion: A Misunderstood Compounder at an Inflection Point

AMD is quietly transforming from being a component supplier to being an AI-native platform orchestrator. Deep operating leverage in conjunction with aggressive system-level integrations and underappreciated developer traction is causing the market to misprice its equity profile. At present prices, AMD presents one of the most skewed setups in the semis: platform economics in a compounder being priced at cyclical levels. As execution reinforces the rack-scale thesis and ROCm scales, the re-rating is not just possible, it's likely.

Recommended Articles