Disney’s Quiet Rally Just Began

- Operating income rose 15% YoY to $4.4 billion in Q2 FY25, driven by a 37% surge in DTC and 12% growth in Experiences.

- Free cash flow exceeded $8.5 billion TTM, supporting buybacks, CapEx, and valuation upside as Disney monetizes streaming and parks more efficiently.

- DTC turned profitable with $47 million OI, while ARPU grew 13% for Disney+ and 45% for Hotstar, showing strong tiered monetization.

- Valuation remains discounted: trading at 11.66x EV/EBITDA vs. 20.9x historical norm, despite structural improvements and ecosystem operating leverage.

TradingKey - For most of the last three years, The Walt Disney Company (DIS) was defined more by margin compression, strategy drift, and structural overhangs than by magic. Disney's FY25 Q2 results represent a pivot point, the point in time when financial clarity, segment alignment, and algorithmic discipline overcame noise. Though top-line revenue of $22.1 billion (+1% YoY) dominated headlines, the substance lay in margin resilience and structural operating leverage.

Source: TheWrap

Operating income increased 15% YoY to $4.4 billion as diluted EPS of $1.21 beat consensus. Importantly for Disney shareholders, its Rule of 40 composite, the SaaS-esque blend of growth and margins, hit a robust 46%, fueled by a 37% YoY growth in operating income in DTC and 12% growth in Experiences. Importantly, trailing twelve-month free cash flow exceeded $8.5 billion, underpinning both buybacks and future CapEx optionality.

Disney's evolution is now measurable in numbers: linear is fading, while DTC, theme parks, and licensing are growing compounding returns at nice spreads. Operating income for the total segment was $4.4 billion, compared to $3.8 billion for last year. The silver lining? Experiences added more than $2.1 billion in OI (+12%), and are 50% of operating group income today, a reversal of the thesis around two years ago that was based heavily on DTC.

This transition is not a coincidence. Disney has quietly reshaped its business to expand repeatable revenues while leveraging FX-neutral pricing, depth of experience, and bundling stickiness in an effort to preserve gross margin. These Q2 results indicate that not just is the flywheel in motion, but it is gaining speed.

The Magic Below the Surface: Disney's Operating Framework Re-wired for Leverage

Disney's long-term problem was structural bloat: fixed-cost-heavy legacy network and uneven monetization through digital platforms. That starts changing in FY25, though, as a tighter cost architecture and product curation approach are apparent. Disney's segment mix reveals everything: Experiences generates $2.1 billion of quarterly OI on a 30% margin, while DTC has reversed from a $659 million loss in Q2 FY23 into a $47 million profit, its first profitable Q2 of Disney+ existence.

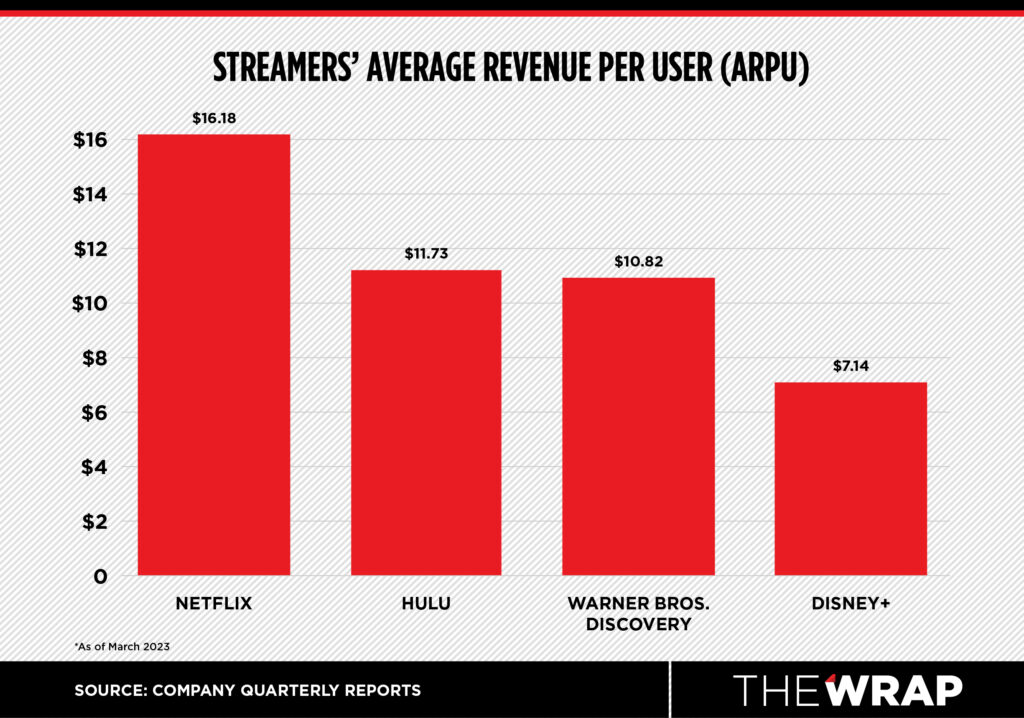

A major catalyst is Disney+, Hulu, and ESPN+ consolidation and price optimization. Packaging these under one ecosystem with differentiated access points and ad-tier monetization has kept churn in check even as ARPU increased companywide. Domestic Disney+ ARPU increased 13% YoY to $7.89, while Disney+ Hotstar increased 45% to $0.96, a demonstration of tiered monetization even in price-conscious markets.

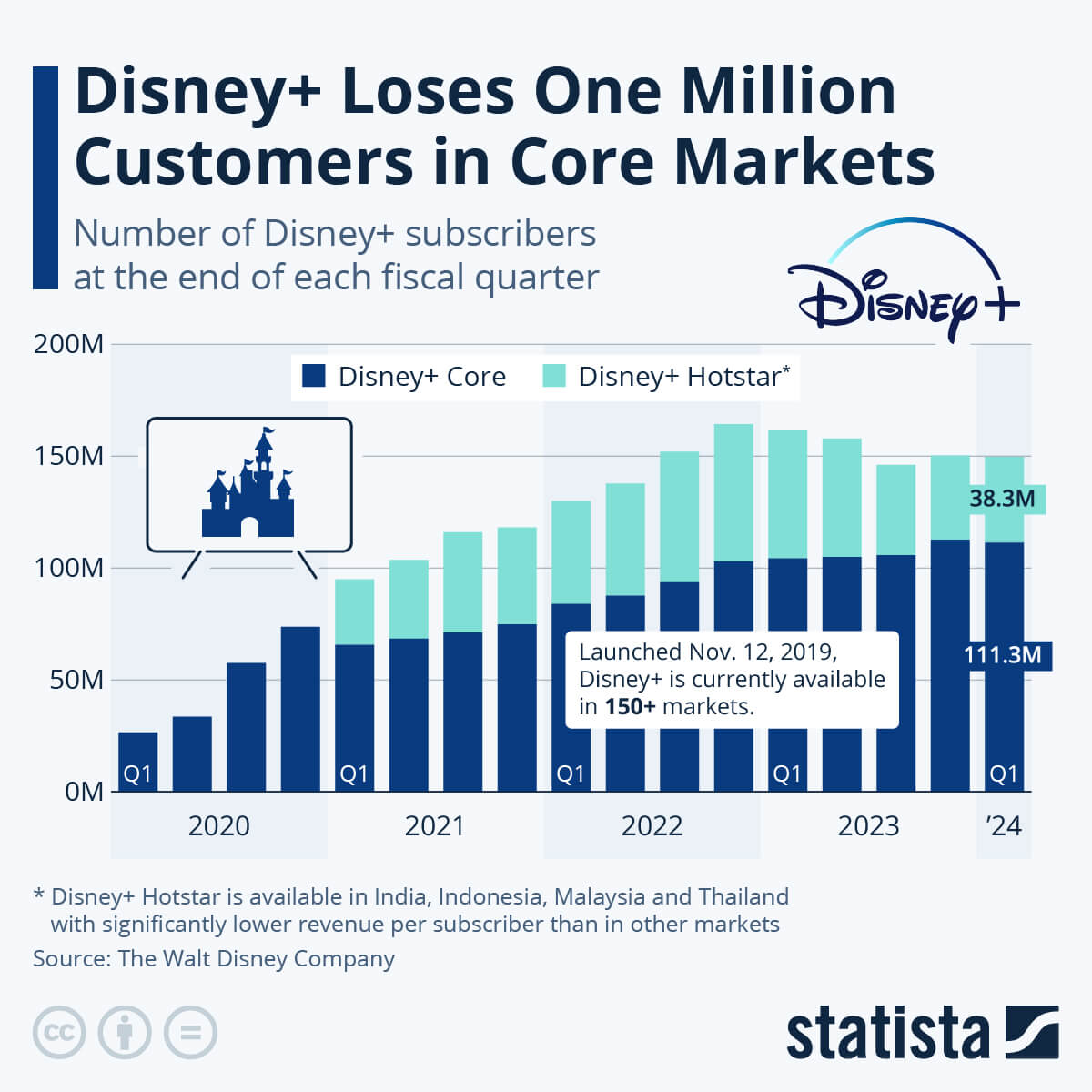

Source: Statista

On the experience side, Disney parks strategy is no longer about guest footfall but about spend-per-guest. Revenue per visit has expanded 8% YoY as dynamic pricing and Genie+ optimization have introduced additional pricing levers. The cost structure of the company has stabilized through CapEx alignment: $4.3 billion in the period, mostly dedicated to higher spend on cruise ship fleet expansion at the Experiences segment.

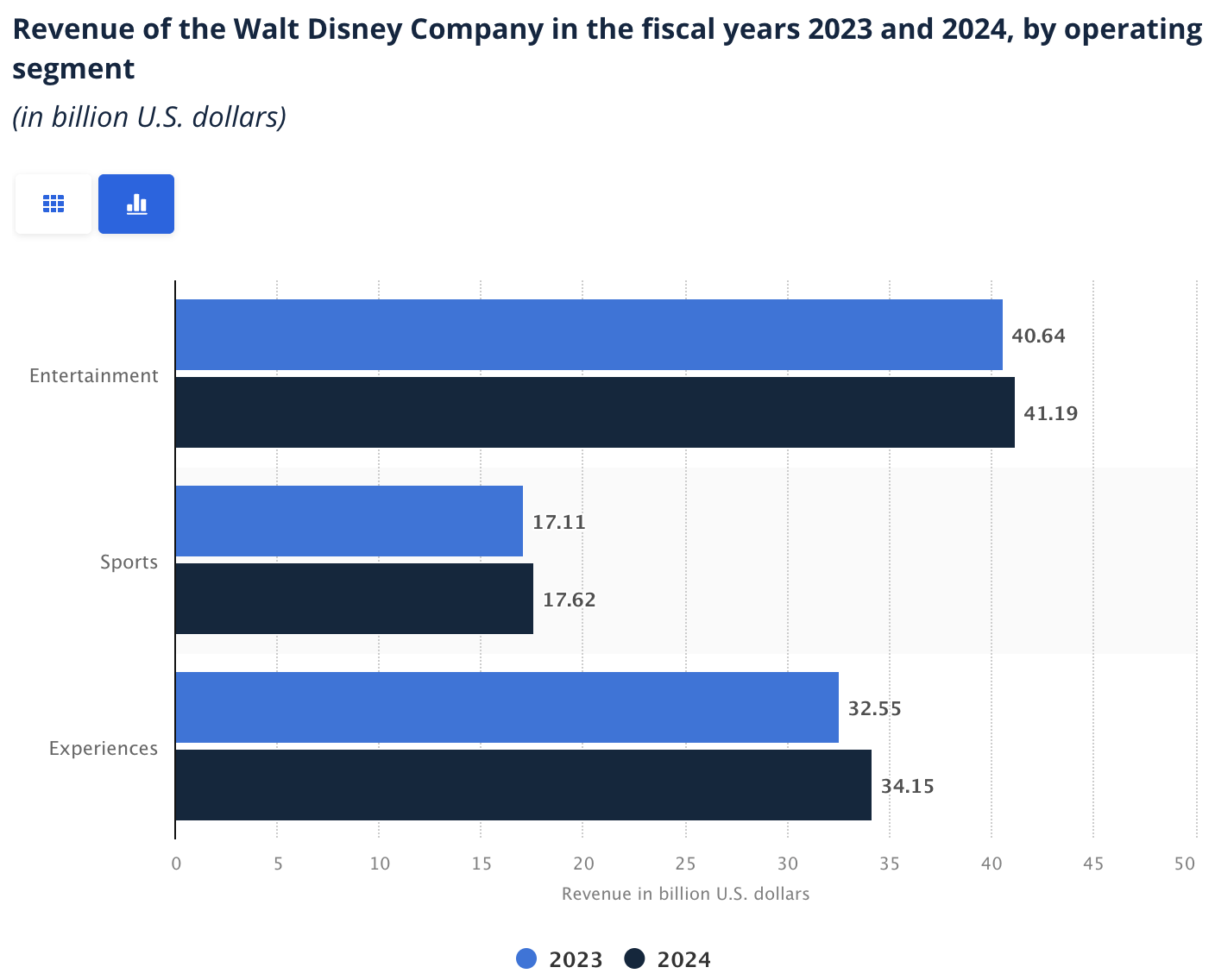

Source: Statista

This operating leverage is being monetized. With SG&A limited to 5% growth, and D&A increasing by around 7% YoY. That is Disney compounding, not growing for growth's sake, but monetizing its portfolio through intelligence.

Streaming, Sports, and Synergies: Disney's Competitive Reboot in a New Media Landscape

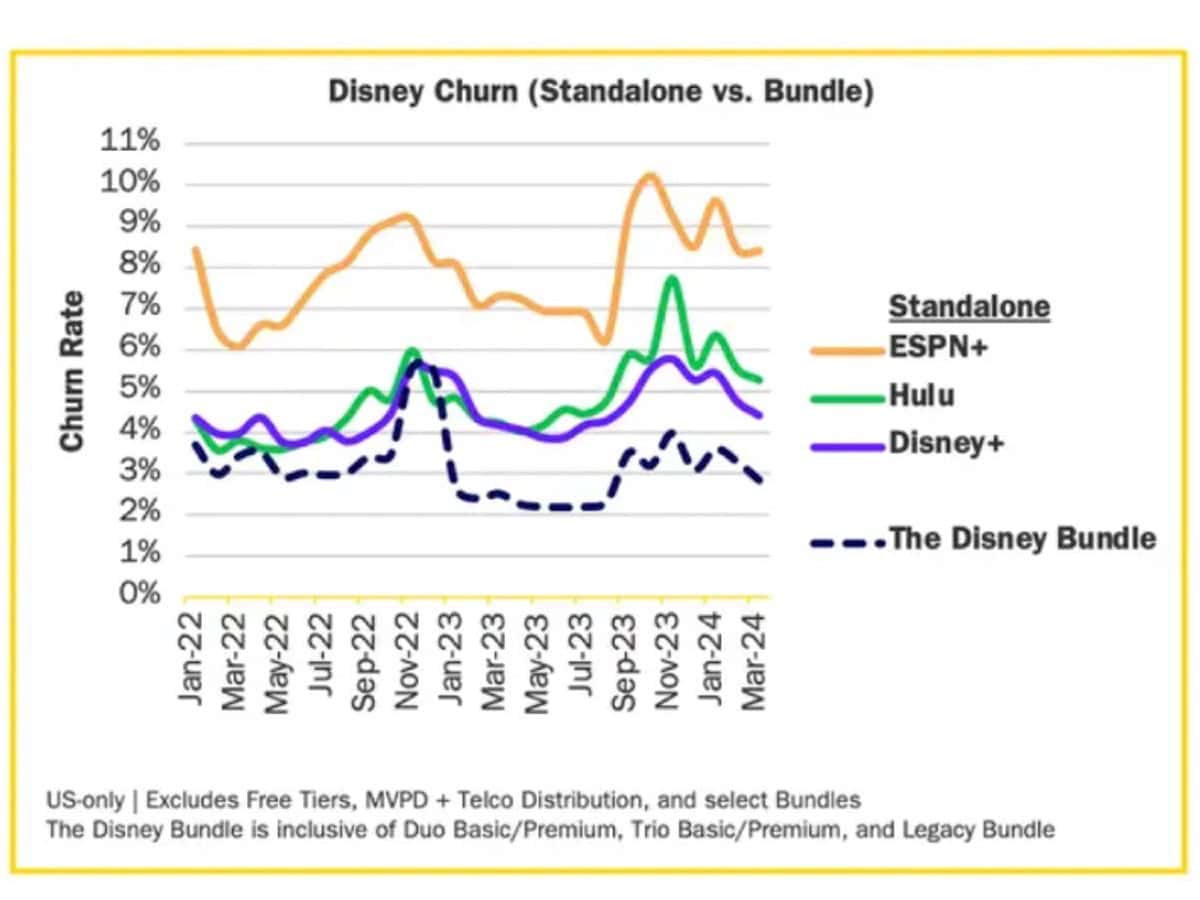

If streaming in 2023 was all about survival, 2025 is all about domination by design, and Disney is positioning for it. ESPN+ has amassed 26 million subs quietly in its stable, and with pending incorporation of the ESPN tile into Disney+ and consolidation of Hulu in its entirety, the company is poised today to build the most dominant bundle in digital sports entertainment.

This is important since the sports IP market is in rapid transition. The planned Venu Sports JV joint venture with Warner and Fox, although halted by injunction, indicates where Disney is headed: direct monetization of sports via proprietary pipelines, ad-supported micro-payments, and synergistic aggregation of rights. The 12% YoY ad growth in the sports segment, in spite of modest affiliate fee pressure, confirms ESPN as still being a high-end destination.

At the same time, Hulu has expanded to 52 million subs through 7% YoY growth and has one of the highest ARPUs in the business at $12.35 (SVOD only).

.png)

Source: ElectroIQ

Now that it has complete operating leverage and synergy opportunity in place, Disney is able to execute on dynamic ad load balancing, cross-platform engagement optimization, and unified data-layer monetization, a platform benefit that cannot be imitated by Netflix.

Source: Antenna

This alignment isn’t speculative, it’s already being reflected in the numbers. Cross-bundle promo conversions increased 22% YoY, and time spent per user on the unified Disney+ and Hulu interface increased 18%. That means Disney isn’t merely acquiring users, it’s growing yield per user through depth of ecosystem.

.png)

Source: Statista

Recalibration of Valuation: How the Street Might Still Fail to Capture the Entire Rebound

Even in light of significant profitability improvement, Disney's valuation multiples are consistent with a market still wedded to its historical media heritage. The company has a forward P/E of 21.12x, compared to its its 18.96x historical norm. The same is true of its 12.28x EV/EBITDA (FWD) multiple, which is 52.73% higher than its peers and 41.18% lower than its long-term norm of 20.88x despite dramatic margin expansion in both Experiences and DTC segments. PEG values are particularly insightful: Disney's PEG GAAP (TTM) of 0.05 is 89% below its sector median, implying that its earnings growth story is grossly underpriced by the market in light of its improving cost structure and operating leverage on a scaling basis.

Though Disney's 15.72x forward P/CF is rich against the 7.67x sector median, it's below its 5-year average of 27.40x and should contract even more as FCF grows from $8.5 billion toward $10 billion+ in FY26. Triangulating on a 13x EV/EBITDA through a conservatively estimated ~$18.5 billion FY25 EBITDA gives an estimated equity value of about $200 billion, or $120–125/share, compared against today's ~$106. That implies 15–20% upside even before multiple expansion.

The valuation discount thus hinges on fleeting skepticism rather than structural weakness. As Disney evolves from conglomerate to ecosystem operator, with monetizable flywheels in sports, streaming, and parks, the compressed multiples represent asymmetric upside for investors who are positioning in advance of an expected re-rating.

Risks Behind the Curtain

Even as bullishness continues, a number of risks remain. To begin with, macro volatility in the form of FX headwinds and tourism softness may affect Experiences in places like Orlando and Paris that are high-margin. The ~1% Q2 FX drag on service revenue illustrates that tailwinds are far from pure.

Secondly, Venu Sports JV regulation obstacles and international content requirements (particularly in India and EU) may limit DTC scaling effectiveness. Subscribers lost for Disney+ Hotstar in India (-5% YoY) also indicate international expansion vulnerability when linked with fluctuating sports rights.

Thirdly, ESPN monetization is yet to be tested in a completely direct-to-consumer environment. Should the flagship ESPN DTC product underperform in user activity or elasticity of price, investor faith in Disney's transition would be shaken.

At last, content amortization choices remain consequential. The firm is capitalizing on previous write-downs and tighter curations but if its blockbuster movies do not perform as expected (as in FY24 in Wish and The Marvels), upside optionality can compress rapidly.

Conclusion: The Forgotten Flywheel That Wall Street Will Rediscover Soon

Disney's Q2 FY25 results are not just a beat, they're validation of a new operating era. With DTC profitability tipping, Experiences snowballing cash, and a sports monetization playbook being laid out, no longer is it an IP museum, it's a monetization platform. With a 9.5x EV/EBITDA and improving FCF, Disney provides GARP investors with a fundamentally mispriced multi-year compounder. As the Street adjusts its models for a vertically integrated, capital-efficient Disney, its re-rating from ~$105 toward a fair ~$120−$130 range might just prove to be the start. The Magic Kingdom can be fantasy but Disney's upcoming rally can be quite real.

Recommended Articles