[IN-DEPTH ANALYSIS] New Zealand: The Impact of Macroeconomic Factors and Monetary Policy on the NZD/USD

Executive Summary

TradingKey - To combat high inflation, the Reserve Bank of New Zealand (RBNZ) aggressively raised interest rates from late 2021 to mid-2023, leading to a technical recession in the New Zealand economy in mid-2024. To stabilize economic growth, the RBNZ initiated a rate-cutting cycle in August 2024, with a cumulative reduction of 225 basis points to date. These significant rate cuts have helped the New Zealand economy begin to stabilize. Looking ahead, with economic recovery underway and inflationary pressures resurfacing, the RBNZ is expected to implement only one additional rate cut by the end of this year. As signs of economic recovery emerge and the pace of RBNZ rate cuts slows, the New Zealand dollar is anticipated to continue appreciating against the U.S. dollar.

Source: TradingKey

* Investors can directly or indirectly invest in the foreign exchange market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Macroeconomic Background

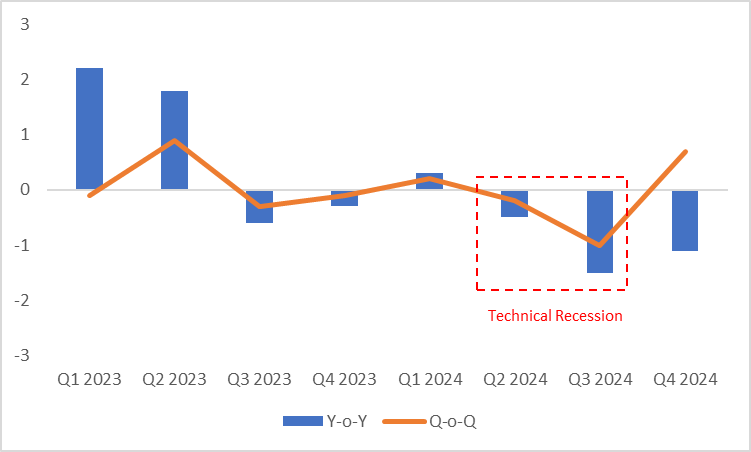

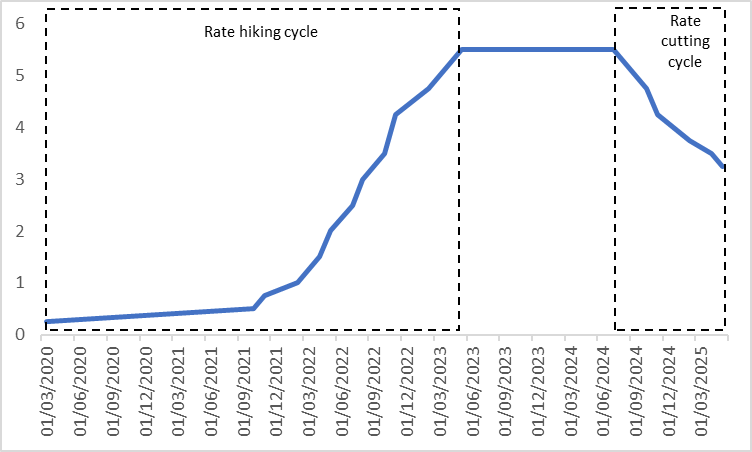

In recent years, the Reserve Bank of New Zealand (RBNZ) has delivered a textbook example of monetary policy management. The pandemic triggered high inflation, prompting the RBNZ to significantly raise interest rates from late 2021 to mid-2023. While inflation was brought under control, the economy entered a technical recession by mid-2024 (Figure 1.1). Against this backdrop, the RBNZ initiated a rate-cutting cycle in August 2024 (Figure 1.2).

Figure 1.1: Real GDP (%)

Source: Refinitiv, TradingKey

Figure 1.2: RBNZ Policy Rate (%)

Source: Refinitiv, TradingKey

2. Recent Macroeconomic Conditions

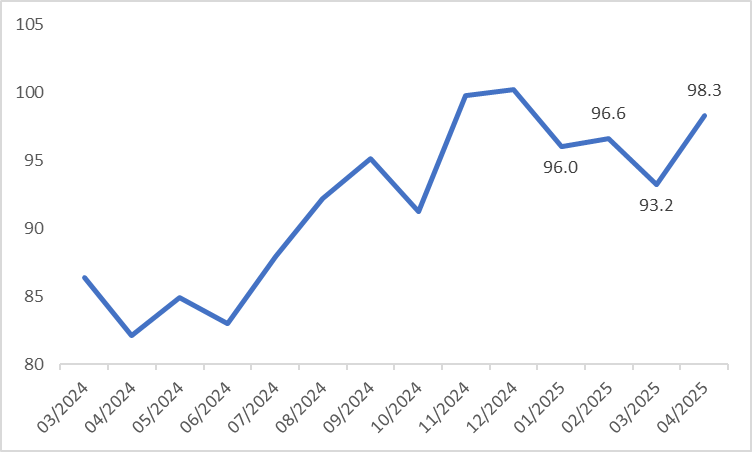

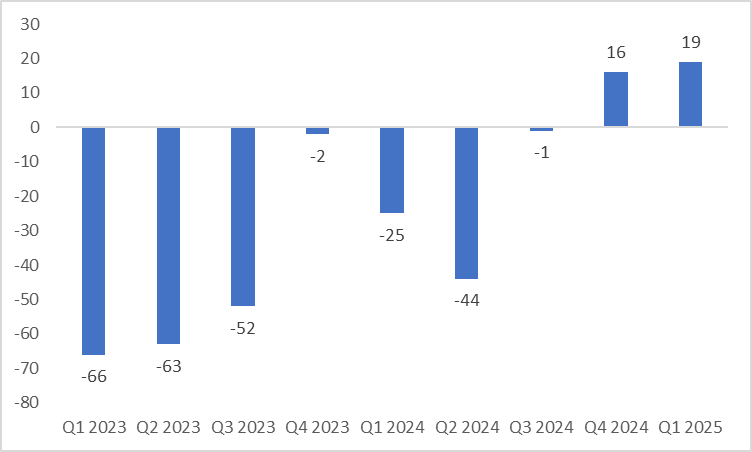

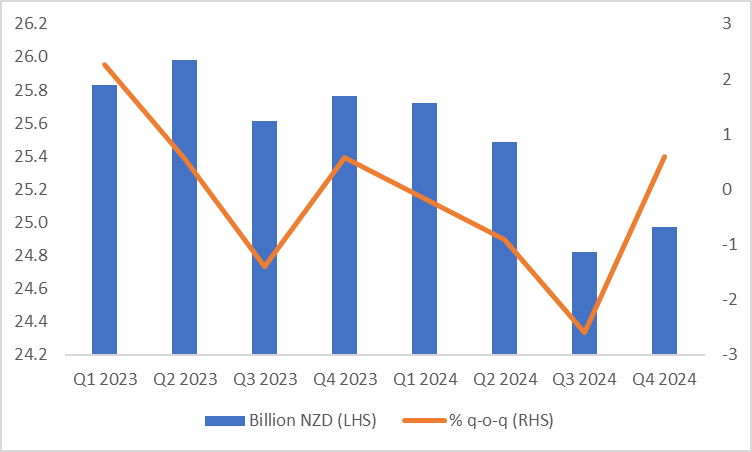

Under an accommodative monetary policy, signs of economic recovery are emerging. Last year's fourth-quarter GDP growth turned positive, recording a 0.7% increase quarter-on-quarter. More specifically, on the consumption side, the Roy Morgan Consumer Confidence index rose to 98.3 in April, higher than the figures from January to March (Figure 2.1). Meanwhile, retail sales have shown positive growth for two consecutive quarters (Figure 2.2). Recovery signals are not only evident in consumption but have also extended to the production side. The NZIER Business Confidence index surged significantly, rising by 16% in the fourth quarter of last year and 19% in the first quarter of this year (Figure 2.3). In addition, driven by improved business confidence, New Zealand's investment has shifted from negative to positive growth quarter-on-quarter (Figure 2.4).

Figure 2.1: Roy Morgan Consumer Confidence

Source: Refinitiv, TradingKey

Figure 2.2: Retail Sales (%)

Source: Refinitiv, TradingKey

Figure 2.3: NZIER Business Confidence (%, q-o-q)

Source: Refinitiv, TradingKey

Figure 2.4: Investment

Source: Refinitiv, TradingKey

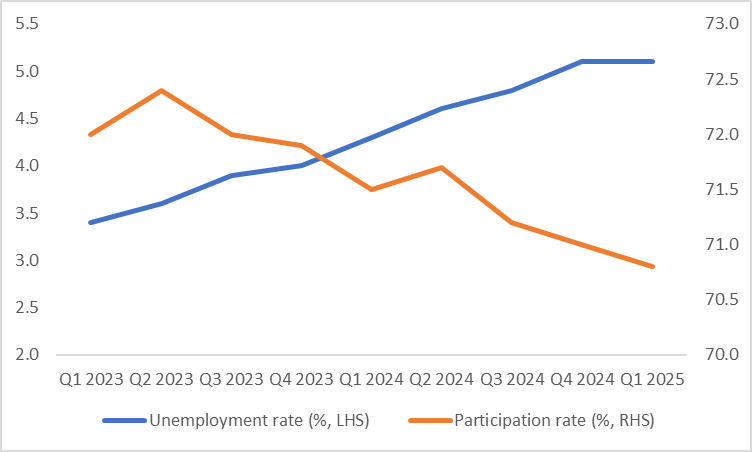

3. Labour Market

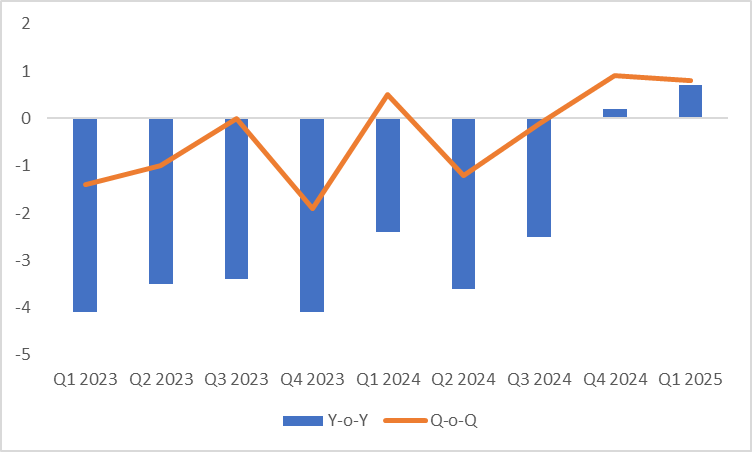

The labour market remains weak, primarily because the recovery in demand takes time to translate into corporate hiring decisions, and employment recovery may lag behind the business cycle. First-quarter data this year shows an unemployment rate of 5.1%, up 1.9 percentage points from the cycle's low and only 0.1 percentage points below the peak during the pandemic. This has led to a decline in the labour force participation rate for several consecutive quarters (Figure 3).

Figure 3: Labour Market

Source: Refinitiv, TradingKey

4. Macroeconomic Outlook

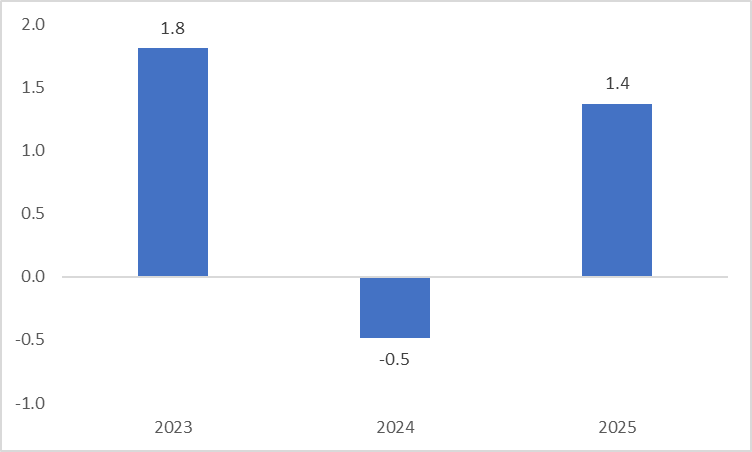

Looking ahead, despite uncertainties in the global economy, we expect New Zealand's economy to continue recovering, driven by a positive consumption-production spiral. The IMF forecasts that New Zealand's real GDP growth will shift from negative to positive, reaching 1.4% in 2025 (Figure 4). Sustained economic growth will benefit the labour market, with the unemployment rate in New Zealand expected to steadily decline in the second half of this year.

Figure 4: IMF Real GDP Forecast (%)

Source: Refinitiv, TradingKey

5. Monetary Policy

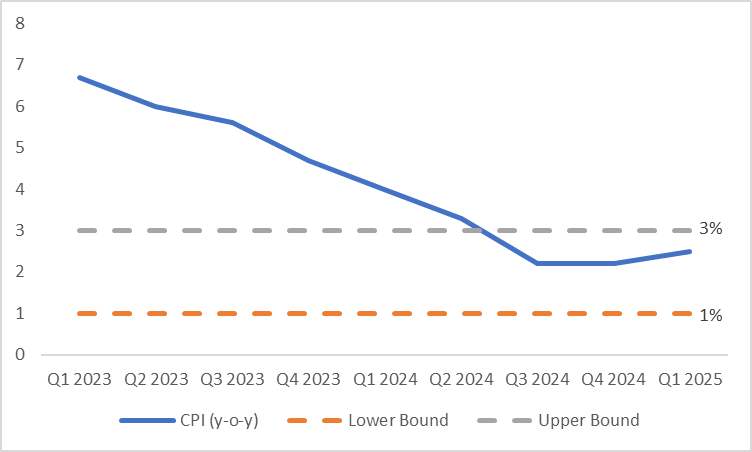

On the inflation front, due to the 2024 economic recession and labour market weakness, New Zealand's CPI has gradually declined, falling back within the Reserve Bank of New Zealand's 1%-3% target range since the third quarter of 2024 (Figure 5). With inflation easing, the RBNZ cut its policy rate by 25 basis points on 28 May 2025, bringing it to 3.25%, marking a cumulative reduction of 225 basis points since August 2024. Looking ahead, with clear signs of economic recovery and rising inflation expectation—CPI rose to 2.5% in the first quarter of this year, up from 2.2% in the fourth quarter of last year—we expect the RBNZ to implement only one additional rate cut before the end of the year.

Figure 5: CPI (%)

Source: Refinitiv, TradingKey

6. Forex

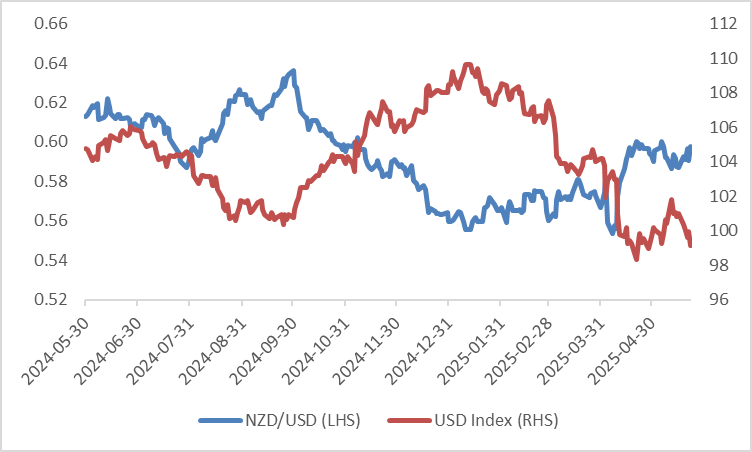

In the first half of April this year, the New Zealand dollar experienced a sharp rally against the U.S. dollar, driven by both domestic and external factors. On the domestic front, the Reserve Bank of New Zealand (RBNZ) gradually adopted a more hawkish stance during April. Concurrently, rising global dairy prices provided support for the recovery of New Zealand's agriculture exporting dependent economy. These two factors combined to bolster the New Zealand dollar's exchange rate. Externally, the U.S. dollar index weakened significantly due to the impact of Trump's tariff policies, further pushing up the NZD/USD exchange rate (Figure 6). Looking ahead, with the economy gradually recovering, inflation showing signs of rising again, and the RBNZ slowing the pace of rate cuts, the New Zealand dollar is expected to continue appreciating against the U.S. dollar.

Figure 6: NZD/USD and USD Index

Source: Refinitiv, TradingKey

Recommended Articles