MARA’s Power Play Behind Bitcoin

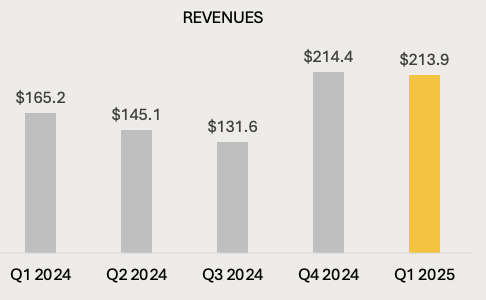

- Q1 2025 revenue reached $214 million, growing 30% YoY, driven by 77% higher average Bitcoin prices.

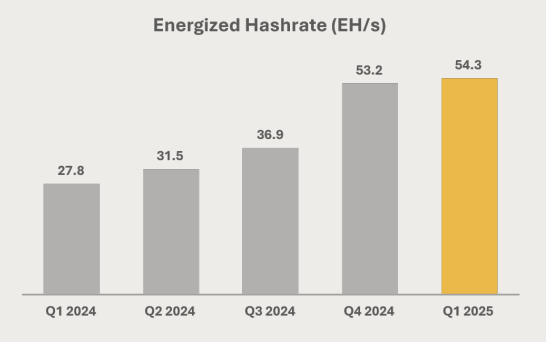

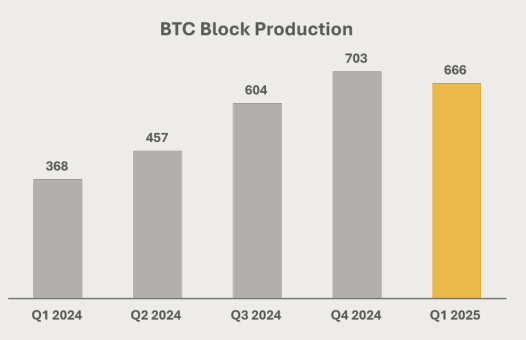

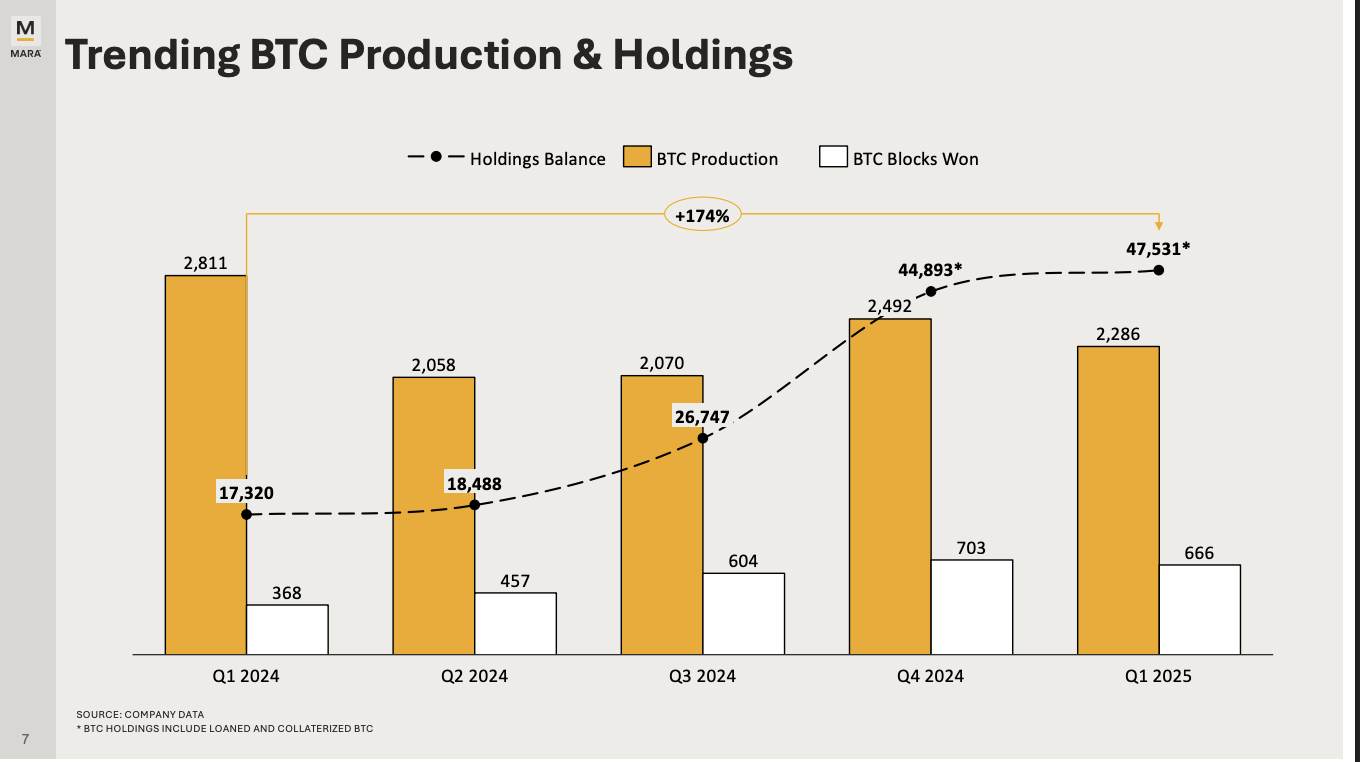

- Hash rate doubled to 54.3 EH/s; block rewards rose 81% to 666 blocks despite post-halving production drop.

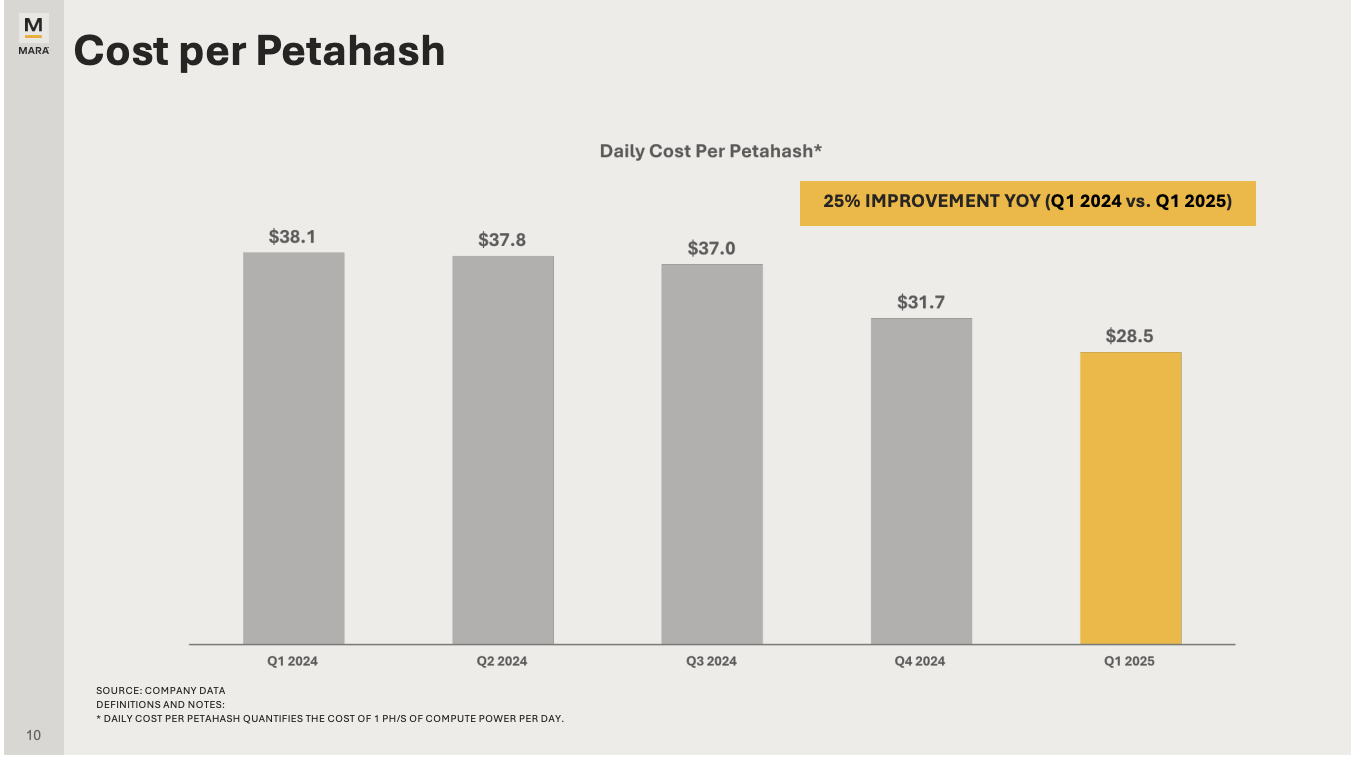

- Cost per petahash fell 25% YoY to $28.5/day; energy cost per BTC mined at operated sites was $35,728.

- Bitcoin holdings reached 47,531 BTC valued at $4.1 billion, increasing 174% YoY and strengthening the balance sheet.

Bitcoin Muscle, Infrastructure Moat: Why MARA’s Strategic Power Play Is Misunderstood

TradingKey - Marathon Digital Holdings (MARA) is no longer simply a high-beta proxy for Bitcoin. Below the surface of disrupted earnings and headline losses is a strategic reshaping that Wall Street is mostly underpricing: MARA is quietly transforming into a vertically integrated digital infrastructure company with a defensible moat in energy. This shift, obscured by GAAP losses incurred through digital asset revaluations, is already delivering structural benefits in cost, scalability, and capital efficiency.

In spite of a headline Q1 2025 net loss of $533 million, primarily a result of a $510 million non-cash markdown of the quarter-end valuation of Bitcoin, MARA's underlying fundamentals speak otherwise. Revenue jumped 30% year-over-year to $214 million, fueled by a 77% increase in average prices of Bitcoin. Hash rate nearly doubled to 54.3 EH/s, while block production rose 81% to 666, eclipsing many of its competitors even in a post-halving mining environment.

Source: MARA Q1 2025 Update

But the true transformation is in the background: from the retrofitting of wind farms in Texas to applying two-phase immersion cooling (2PIC) for upcoming AI workloads, MARA is becoming a digital power utility, not merely a miner.

The market is punishing MARA for the volatility in BTC-related earnings while overlooking the intrinsic optionality in its power infrastructure ownership, modulized data centers, and vertically integrated cost disciplines. It holds 47,531 BTC on the balance sheet (valued at Q1-end at $4.1 billion), providing scarce equity exposure to stranded energy monetization and long-duration upside in Bitcoin.

The valuation squeeze on the stock may be a short-term FUD reflection, but it does provide an opening to re-rate over the longer term as the company transformation story gains steam.

Beyond the Hash: From Miner to Modular Utility

MARA's model is now less about hash-race scale and increasingly about strategic power leverage. In Q1's report, we find a company leaving behind the arms race of hardware deployment and embracing the economics of power sovereignty. This is an important distinction. While competitors such as Riot and CleanSpark are still perusing petahash targets through capex-intensive ASIC deployments or hosting agreements, MARA is constructing a proprietary power stack, buying, operating, and consolidating its own renewable and flare gas power assets.

This model is already demonstrating capital efficiency. Its newly acquired 114 MW Texas wind farm, bought at ~$205K/MW, will provide generation at sub-$30/MWh in grid-connected mode. That is well under the industry average and allows MARA to profitably continue running legacy ASICs, where it's extending their life cycle and delaying upgrade costs. In addition, MARA's gas-to-power assets in North Dakota and Texas have the lowest BTC generation costs in its fleet while having 99% methane abatement, providing both ESG arbitrage and operating alpha.

Notably, MARA's verticalization encompasses transformation infrastructure, not merely generation. A 50 MW expansion in Ohio was on schedule, and the company's expanding capabilities in immersion-cooled modular data centers place it well to handle not only Bitcoin mining but future AI inference demand. This is not merely branding. MARA's in-house developed 2PIC cooling infrastructure allows thermal efficiency and waterless scaling, something that is necessary since high-density compute nodes need infrastructure that hyperscalers are finding it ever more difficult to provide.

The result is a company less focused on Bitcoin's block reward structure and more focused on platform economics: commoditizing energy-to-compute conversion at scale and at the edge. This shift makes MARA less of a miner and more of a compute utility company designed for economic arbitrage, AI workload flexibility, and volatility in power.

Block Rewards, Balance Sheets, and Burn Rates

The profitability tells a story of bifurcation, headline losses hiding operating leverage in the making. Q1 2025 revenues reached $213.9 million, a 30% YoY increase, even with a sequential 8% drop in BTC production caused by the April 2024 halving.

Source: MARA Q1 2025 Update

What supported this? Block rewards rose 81% to 666, even with less BTC mined, due to the contribution from MARA Pool and transaction fee optimization. Having its own pool allowed MARA to keep 100% of fees, increasing the per-BTC revenue over network averages.

Source: MARA Q1 2025 Update

Simultaneously, cost control is improving structurally. Cost per petahash declined 25% YoY to $28.5/day and 10% sequentially, fueled by a fleet composed of 60% of rigs with a hashing power of less than 20 J/TH. G&A per petahash decreased 40% sequentially, no easy task in a scaling, capital-intensive business. Energy cost per BTC at operated sites stood at $35,728, a competitive rate in the face of grid volatility.

Source: MARA Q1 2025 Update

In addition, MARA controls $4.1 billion in cash and BTC, including 47,531 BTC, an increase of 174% YoY, reflecting a fortress balance sheet in a class of its own in the industry. The market is nonetheless obsessed with the -$533 million net loss and -$484 million adjusted EBITDA, both of which were distortions due to mark-to-market losses. Of note, a post-quarter recovery in BTC to ~$100,000 would represent a $500 million swing in fair value, reversing the Q1 loss on the books.

Source: MARA Q1 2025 Update

Volatility is a characteristic, not a glitch, of MARA's “BTC as treasury” model, but obscures real earnings power. Critically, Marathon raised $100 million through ATM in Q1 but started a new $2 billion ATM program. While this is dilutive to shareholders, the financing comes at sector-low multiples. Capex-per-MW is still 28% lower than peers such as CleanSpark and Riot, and the strategic issuance of shares to finance ROCE-enhancing asset expansion to date maintained balance sheet flexibility.

Valuation: Where BTC Yield Intersects with Infrastructure Alpha

Analyzing MARA in traditional P/E or EBITDA terms misses the value embedded in its double-flywheel model: treasury BTC appreciation and cost-effective infrastructure monetization. As of 31 Mar, the fully diluted BTC yield per share of 100 BTC per million shares is triple the industry's next best miner. This metric is crucial. It suggests shareholders are not merely investing in exposure to operating income but also BTC-denominated NAV, with upside correlated to macro adoption of digital gold.

Using a sum-of-the-parts methodology, consider MARA's BTC holding value at $100,000 BTC (near-spot): 47,531 BTC represents NAV of $4.75 billion, or $10/share. Add a quarterly revenue run rate of $860 million annualized to $214 million, and apply a modest 35% margin at scale, and MARA is capable of producing $300 million+ in EBITDA ex-mark-to-market volatility.

Project a 12x EBITDA multiple into an energy-infrastructure-like business, and you get ~$3.6 billion in enterprise value excluding BTC. On a fully diluted 475 million share count, the weighted-average valuation drives intrinsic value to $17–$18/share, potentially with upside should BTC move above $120K or AI compute services commence in 2025.

Peers such as CleanSpark and Riot sell at advanced forward EV/sales multiples despite having weaker treasuries, lower self-mined BTC per share, and greater third-party hosting dependencies. MARA's valuation discount is becoming ever more challenging to rationalize. The exception? This valuation is based on persistent BTC price support and effective recycling of capital. Excessive ATM dilution remains a concern. Yet, MARA's transforming business model is one of resilience compared to its peers, especially inasmuch as it is starting to monetize behind-the-meter power, heat recovery, and potentially AI inference hosting.

Risks, Not Red Flags: Volatility with a Thesis

MARA's greatest danger is exactly why it has asymmetric upside: exposure to price fluctuations in BTC. It holds $4.1 billion in BTC and reported a Q1 quarter with an unrealized Q1 loss of $510 million. The income statement will continue to be noisy. A BTC move of $10,000 can move net income by ~$500 million, a volatility tax the market hasn't yet priced sensibly.

Second, its model remains disproportionately based on ATM issuance. Although MARA exhibits excellent ROCE and CapEx discipline, ongoing equity raises threaten shareholder dilution unless mitigated by significant EBITDA expansion or BTC price appreciation. Increasing G&A expense, although reducing per hash, nonetheless doubled year on year in dollar terms due to staff expansion and increasing complexity of operations.

Lastly, AI monetization is still in the form of storytelling, with narrow pilots in progress but no real revenue booked so far. If MARA is not successful in transforming its infrastructure into a wider compute-as-a-service offering, the vertical integration thesis may be halted at the BTC mining level. But those are execution, not viability, risks. Its structural strengths in energy, infrastructure ownership, and modularity provide cover that much of its more asset-light or hosting-based competitors lack.

Conclusion: A Disputed Protocol-to-Use Transition

MARA's evolution into a vertically integrated digital company is in plain sight. While Bitcoin-correlated volatility obscures its profitability optics, the company is systematically constructing a high-efficiency, low-cost infrastructure stack that makes money from compute rather than coin.

As the industry consolidates and compute demand broadens to inference and edge workloads, MARA's hybrid infrastructure-treasury model can potentially trigger a re-rating. For long-term investors willing to stomach volatility, MARA is not just a Bitcoin mining company but an underappreciated call option on the convergence of power, compute, and protocol-based monetization. Priced where it is today, it is perhaps one of the only means in existence to acquire digital infrastructure at a discount to its digital value.

Get started

Recommended Articles