Nvidia Q1 FY2026 Earnings Preview: Navigating Peak AI Optimism Amid Valuation Gravity

- Nvidia's FY2025 revenue hit $130.5B with 90% from compute and networking; net income soared to $72.88B.

- Gross margin reached 75%, but $3.7B in inventory commitments and $5B in stock comp signal emerging cost pressures.

- Forward P/E of 32.31x reflects perfection pricing; base-case value is $131, with downside to $96 if growth slows.

- Blackwell chips and $3.4B CapEx ramp support long-term AI platform push, blending silicon with high-margin software offerings.

Nvidia (NVDA) heads into its May 28, 2025, Q1 FY2026 earnings release with the weight of stratospheric expectations and an unmatched run of performance. Its dominance in AI infrastructure has rewritten the script for the semiconductor industry, but cracks are now appearing in the assumptions driving its valuation.

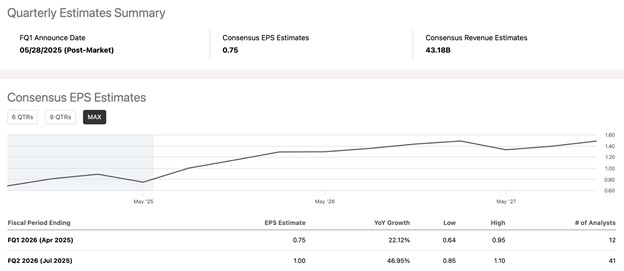

Eight consecutive beats on the bottom line and an identical record on revenue surprises have made the stock AI optimistic in name. Analysts project $0.75 in earnings on $43.2 billion in revenue, both astronomical year-over-year gains. But as the momentum on earnings starts to normalize and valuation squeezing gets closer, the Q1 print can be the fulcrum for how markets discern hardness from exuberance.

Source: Seeking Alpha

The firm has beat estimates each of the past four quarters, most recently beating Q4 2025 by $0.04 on EPS and $1.19 billion on revenue. Analysts expect year-over-year EPS growth of 22.12% this quarter as momentum accelerates rapidly through the fiscal year. EPS growth of 47% in Q2, 41% in Q3, and 45% in Q4 indicates the persisting strength of Nvidia’s AI-driven cycle of demand and data center monetization.

Beyond the quarter, Nvidia's growth profile remains attractive on a forward basis. FY2026 full-year EPS is estimated at $4.11 and grows to $5.65 in FY2027, 37% annualized growth. Revenue estimates jump from $199.8 billion in FY2026 to $247.3 billion in FY2027. The shares remain trading at a FY2026 forward P/E of 32.08x and a FY2027 forward P/E multiple of 23.34x and may offer room for multiple expansion if earnings visibility improves.

The upcoming earnings report will be under close examination for AI infrastructure demand growth, Blackwell GPU ramp progress, and increasing expansion in the enterprise and sovereign cloud verticals. Evidence of sustainable pricing and FCF conversion will be important triggers for a re-rating.

Source: Nvidia Company Overview, February 2025

The AI Monolith: Compute at Scale, Margin at Peak

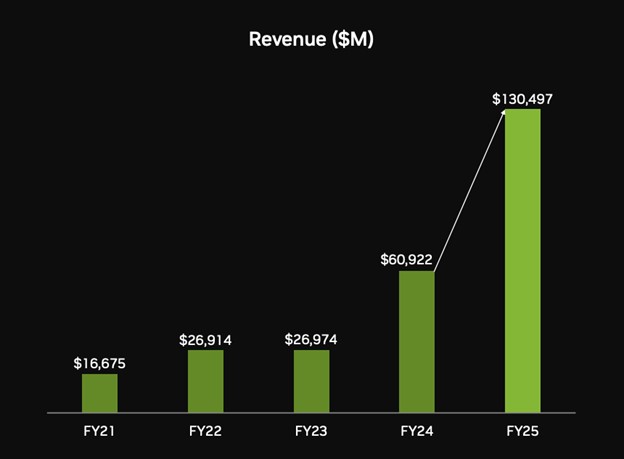

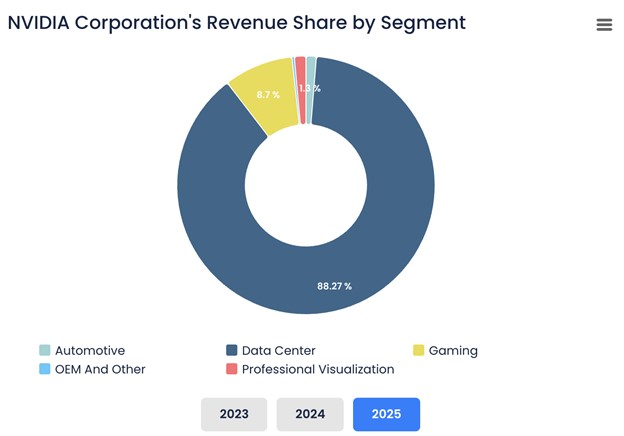

Nvidia's entire-scale transformation from being a GPU vendor to the world's backbone of AI computation is reflected in its fiscal 2025 performance. Revenue doubled to $130.5 billion and net income shot up to $72.88 billion, records in the industry. The Compute & Networking business segment, generating revenue from its AI-driven accelerators, contributed $116.2 billion in revenue, nearly 90% of the company's overall revenue and growing 145% year-on-year. These numbers not only point to strong demand but the entire shift of global data center structure in favor of Nvidia.

Source: BullFincher

Gross margins improved to 75% due to a product mix heavily skewed in favor of high-end Hopper-based GPUs sold to hyperscalers as well as sovereign buyers. The profit performance here indicates strong pricing power, but in it lie nascent weaknesses. Higher inventory provisions and purchase commitments reached $3.7 billion, indicative of forward price bets starting to get aggressive. The risk is not whether the company continues to expand, it most certainly will do so, but whether it can sustain this profitability profile as cost pressures build and competition gets fiercer.

The new Blackwell architecture coming into the shipping stage can support the demand cycle but put pressure on pricing power as hyperscalers increase custom chip production and try to diversify out of Nvidia's vertically integrated high-end stack. The company's success has put it in the position of margin setter and market maker, but also in the crosshairs of customers looking at alternatives.

Blackwell Flywheel of capital expenditures, CapEx Flywheel

At the heart of Nvidia's optimistic thesis is the coming together of several secular long-term factors. The Blackwell launch in Q4 FY2025 has the potential to trigger another wave of sovereign and enterprise AI spend. Hyperscalers and nation-states are each re-architecting infrastructure to support LLM training, AI agents, and simulation workloads, each of which Nvidia is well-positioned to support.

Aside from silicon, the business is quickly creating a software and services moat. Its AI Enterprise suite of software and services, DGX Cloud, and vertical platforms such as Clara (healthcare) and Omniverse (industrial simulation) are pushing towards a hybrid monetization strategy melding hardware with recurring software revenue. The shift from chip maker to platform orchestrator is also reflected in organizational strategy as more than half of the engineers at Nvidia work on software.

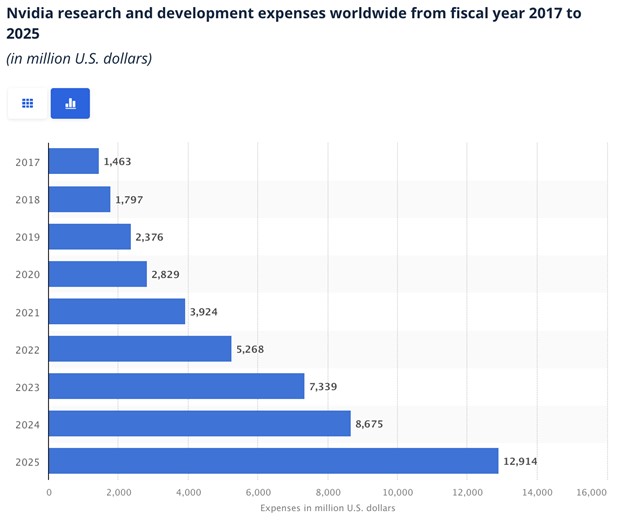

Capital spending jumped to $3.4 billion in FY2025, over three times the amount spent in the prior year. The CapEx ramp-up indicates the company's long-term confidence in sustained demand as it expands manufacturing alliances, supply chain capacity, and internal compute for development purposes. The bet is obvious: controlling more of the stack, both hardware and software, has compounding returns through platform lock-in, ecosystem leverage, and higher margins.

The short-term opportunity lies in the Blackwell upgrade cycle and increasing enterprise demand. The deeper thesis is, however, predicated on the ability of Nvidia to monetize its AI infrastructure through recurring revenue. The issue confronting investors is not whether or not the next GPU cycle goes to Nvidia but whether the wins translate to structural cash flow benefits and economic sustainability for the decade.

Source: Statista

Competitive Pressures, Macro Factors, and Margin Pressures

Although Nvidia moves from strength to strength, signs start to indicate its competitive moat will start to thin. AMD's MI300X gains ground in inference workloads in price-conscious environments. At the same time, cloud vendors are scaling in-house chip abilities, Amazon's Trainium and Google's TPU have evolved as serious competition for specific use cases. The longer hyperscalers use Nvidia's high-end stack, the more incentive for them to innovate against it.

Export controls also pose an increasing source of risk. With U.S. high-performance GPU exports to China and other geopolitically exposed regions prohibited, the total addressable market for Nvidia may be constrained. Increased policy enforcement and localization of the supply base can diminish the company's global optionality in terms of revenue.

Source: GrandViewResearch

In addition, certain of the financial strength in FY2025 of Nvidia is indicative of high risk-taking. Inventory charges have surged, and stock compensation has come in at almost $5 billion, two of the only potential pressure points on margins if not well managed. Although gross and operating margins are the envy of the sector, the issue is whether these are structural bottoms or cyclical tops.

Nvidia also has to contend with a changing macro environment. Increases in interest rates and reduced IT budgets in corporations can provide roadblocks to enterprise AI takeup at least in non-hyperscaler environments. The company's destiny can be held in the hands of CapEx spend across a small number of high-value customers, concentration risk too easily ignored in the context of hypergrowth.

Valuation Outlook: Anchoring Price to Realized Earnings Power

The share price today appears to be valuing a world in which the company continues to operate flawlessly in silicon, software, and systems. At 32.31x forward P/E, the market is assuming significant premium growth runway with little disruption. Working back from FY2026's $4.37 in estimated earnings implies base-case value in the neighborhood of $131 a share, in line with where it happens to be trading today. If growth decelerates and the market starts to bring valuations back to sector means (22x forward earnings), risk of the downside to ~$96 appears.

Conversely, using a 29% growth rate and 1.0 PEG ratio for FY2027 EPS of $5.65 suggests upside potential nearer $164 on the assumption of margin sustainability and ongoing AI adoption. The stock continues to be a high-conviction long-term hold for growth-minded investors, but one that is extremely susceptible to changes in the story. Now that valuations can no longer be expanding, earnings need to keep doing the heavy lifting. From the high-revenue and margin base, even small disappointments could bring about rapid repricing.

Conclusion

Nvidia reports into its Q1 FY2026 earnings with unprecedented momentum but carries the burden of expectations and valuations requiring nothing less than perfection. The company is structurally well-positioned in the race to AI infrastructure, but the margin for error is thin. The second part of the journey will rely not just on continuing growth, but on the willingness of the market to have faith that the best is yet to come.

Recommended Articles