Costco Earnings Preview: A Valuation Stress Test of Resilient Pricing

TradingKey - Costco ( COST.US) will release its fiscal 2026 third-quarter earnings after the U.S. market close on May 28. The market expects revenue of approximately $69.3 billion, a 9% year-on-year increase, and adjusted earnings per share of approximately $4.56, a 13% year-on-year increase.

Previously in the second quarter, Costco delivered a double-beat performance with revenue of $69.6 billion (up 9.2% year-on-year) and earnings per share of $4.58. Oil Prices and the U.S.-Iran Situation: Uncertainty is mounting on both fronts.

Inflation, tariffs, and the Middle East situation are simultaneously weighing on both consumers and businesses. In the first quarter, Walmart's operating profit was dragged down by approximately 250 basis points due to high fuel costs, warning of a common risk for all major retailers. Goldman Sachs' latest macroeconomic forecast raised the probability of a U.S. recession in the next 12 months from 10% to 15%. Costco has previously expressed concern about the Middle East situation affecting fuel costs and shipping schedules, as oil prices near $100 per barrel erode the profit buffers of its already lean low-price operating model.

However, Costco's model is inherently resilient when facing "consumption downgrading." Bank of America analysts noted that while surging gasoline prices squeeze gas station margins in the short term, persistent high oil prices tend to drive price-sensitive consumers toward Costco, which is renowned for its "low-price gas station + warehouse store" combination. Roughly 50% of members shop in the store while refueling; this cross-selling mechanism allows high oil prices to potentially act as a catalyst for net foot traffic.

Membership stickiness remains the primary source of profitability.

Second-quarter membership fee revenue reached $1.36 billion, a 13.6% increase year-over-year, beating market expectations. Renewal rates in the U.S. and Canada reached 92.1%, while the global renewal rate stood at 89.7%. Management attributed minor fluctuations in renewal rates to increased online market share accelerating penetration among younger members, a structural adjustment that is conducive to customer base expansion in the long run.

April sales data further reinforced the trajectory of same-store sales growth.

For the four-week period ending May 3, overall same-store sales surged 11.6% year-over-year, with the U.S. market recording 11.7% and Canada and other international markets growing by 11.5% each. After excluding the impact of gasoline prices and currency fluctuations, adjusted same-store sales growth remained solid at 7.8% (8% in the U.S. and 7.6% in Canada), indicating that growth was primarily driven by higher shopping frequency and average transaction value rather than purely by inflation.

E-commerce is emerging as a second growth engine. Comparable e-commerce sales rose 22.6% in the second quarter, with online comparable growth in April alone reaching 18.8%. The synergy between online and offline channels is enhancing customer stickiness and repeat purchase rates.

Store expansion is also progressing steadily. By the end of the second quarter, the total global store count reached 924, with a full-year target of approximately 28 net new openings and plans to maintain a pace of over 30 net new stores annually in the coming years. A longer growth runway implies continued room for the revenue ceiling to rise.

Valuation overextension is the core conflict for Costco.

Costco's current forward P/E ratio is approximately 53x, significantly higher than the peer average.

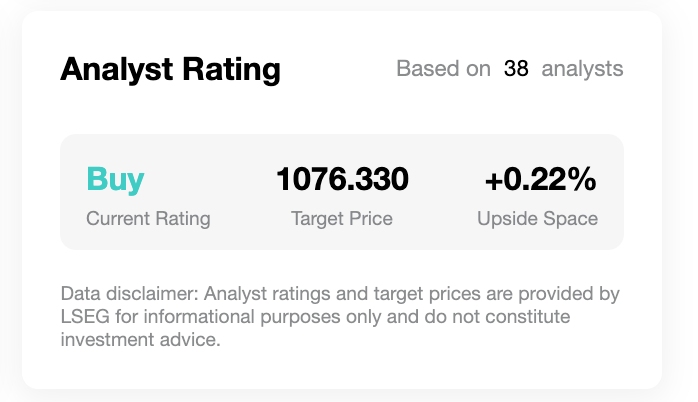

[Analyst Ratings and Target Prices, Source: TradingKey, LSEG]

The average price target from 34 Wall Street analysts is approximately $1,076, implying only about 4% upside from the current share price of roughly $1,028, reflecting institutional optimism about fundamentals but general caution regarding further upside.

Ahead of the earnings release, Oppenheimer lowered its earnings forecast, projecting third-quarter EPS of $4.75, which is below the Wall Street average estimate of approximately $4.98,

attributing this to a "transient earnings dip" caused by a mix of factors in its fuel, e-commerce, and pharmacy businesses. This view touches upon structural bottlenecks in Costco's model: under the triple pressure of maintaining low prices, rising fulfillment costs for online orders, and historically high fuel costs, any change in short-term margins could prompt a downward valuation revision by the market.

Historical earnings beat rates warrant continued monitoring; over the past eight quarters, Costco has met analyst expectations for both revenue and EPS seven times, indicating a high degree of earnings predictability.

Costco's solid fundamentals themselves face no fundamental challenges; the question is whether these fundamentals can support a share price where high valuations are already priced in. Each earnings season serves as a stress test for the market to re-examine this baseline.

Recommended Articles