Is Alphabet Stock Still a Bargain?

Key Points

Alphabet's stock has reached a premium valuation point.

Alphabet continues to post excellent results, proving it deserves that premium valuation.

- 10 stocks we like better than Alphabet ›

Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) stock has had a strong rally since April began. The stock has risen more than 33% since then, which may have investors wondering if Alphabet stock is still a bargain, as it was a few months ago.

Let's take a look at a few valuation measures and see if Alphabet is a buy right now or if investors should move their investment dollars elsewhere.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

Alphabet has gone from a laughingstock to a market leader

Alphabet wasn't the artificial intelligence (AI) leader it is today at this time last year. The market was concerned that AI was going to obliterate its Google Search business and that Alphabet's generative AI models (Gemini) couldn't stand up to the competition. That thesis has proven to be false so far. Google Search has transformed into an AI-first platform, with most searches now offering AI-powered summaries that enhance the overall product experience. Gemini has proven itself to be a leading AI model and can stand with some of the most prominent AI start-ups.

As a result, its valuation has increased thanks to improving confidence.

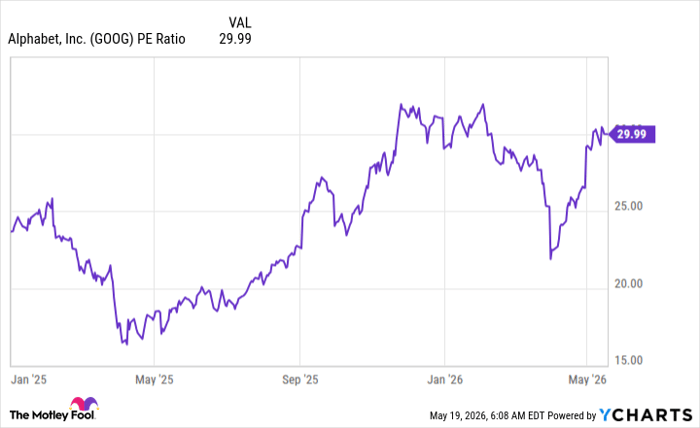

GOOG PE Ratio data by YCharts

Alphabet's price-to-earnings ratio has nearly doubled from its lows in April 2025, which may make investors concerned about its future. However, 30 times earnings has been the usual high-end range for best-in-class big tech stocks. For reference, Apple (NASDAQ: AAPL) and Amazon (NASDAQ: AMZN) trade for 36 and 32 times earnings, respectively. So Alphabet may not be expensive, but it certainly isn't cheap.

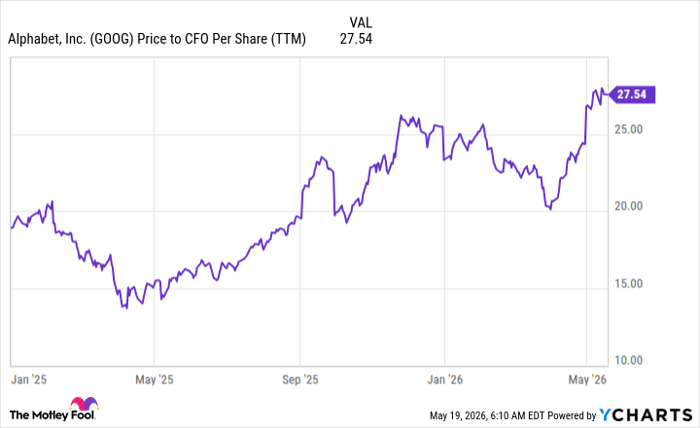

However, earnings can be affected by many things, including investment gains, one-time tax effects, and depreciation after a major capital expenditure. All three of those apply to Alphabet, and it may be helpful to look at the business in terms of operational cash flow.

GOOG Price to CFO Per Share (TTM) data by YCharts

By this metric, Alphabet is the most expensive it has been in the past decade. Now, other companies trade in this same range, but they are expensively valued. So I think Alphabet is fully valued, which means that any future upside must come from business growth. Fortunately, Alphabet grew its revenue at an outstanding 22% pace this past quarter. That's much faster than the market's 10% average, which means Alphabet is still a solid stock to buy and hold on to -- it's just not as good a value as it once was.

Should you buy stock in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $477,813!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,320,088!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 24, 2026.

Keithen Drury has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, and Apple. The Motley Fool has a disclosure policy.

Recommended Articles