Prediction: Micron Technology Stock Will Be Worth at Least $1,500 in 1 Year.

Key Points

Shares of Micron Technology are surging as growth investors increasingly recognize the importance of memory in the AI chip stack.

Wall Street expects Micron's earnings to almost double over the next year.

Despite accelerating sales and explosive profits, Micron trades at a modest valuation based on forward earnings.

- 10 stocks we like better than Micron Technology ›

Micron Technology (NASDAQ: MU) has witnessed a jaw-dropping surge in its stock price over the past month, rising from $448 to a peak of $804. That run-up reflected growing excitement around artificial intelligence (AI) and the critical roles that DRAM and NAND memory chips play in next-generation data centers.

As hyperscalers accelerate their investments into AI infrastructure, demand for advanced memory solutions has risen sharply, to levels well in excess of supply. Micron's ability to deliver strong revenue and earnings results amid this memory supercycle has shifted sentiment -- turning what was once viewed as a cyclical commodity player into a company that is now viewed as a key enabler of the AI boom.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

What fueled Micron's recent surge?

The parabolic move in Micron's stock stemmed from exploding demand for high-bandwidth memory (HBM) and other advanced DRAM and NAND products. GPUs and other AI processors need rapid access to large volumes of data when they are training and deploying large language models (LLMs), and Micron's offerings can supply that.

As AI data center operators face intensifying pressure to scale up their computing capacity, one of the bottlenecks controlling the pace of their build-outs is the available supply of specialized memory. This environment has allowed Micron to command strong pricing power, expand its footprint in AI data centers, and grow both revenue and profits impressively.

What does Micron's growth trajectory look like?

The traditional boom-and-bust pattern in the memory market arises from the nature of the business. Memory-chip makers engage in heavy capital investments to add production capacity during periods of higher demand, but it takes a few years to get those new factories up and running. The combination of that lag and the moves of all the competitors in the space to boost their capacity has always led to periods of oversupply that result in slumping prices -- collapses that can be exacerbated if consumers and enterprises broadly choose not to upgrade their devices, further sapping demand.

However, the AI revolution has introduced meaningful secular tailwinds that should alleviate some of the cyclical volatility. Expanding AI workloads, the rise of autonomous vehicles and robotics, and the introduction of agentic AI should provide a more robust floor for memory demand compared to past cycles.

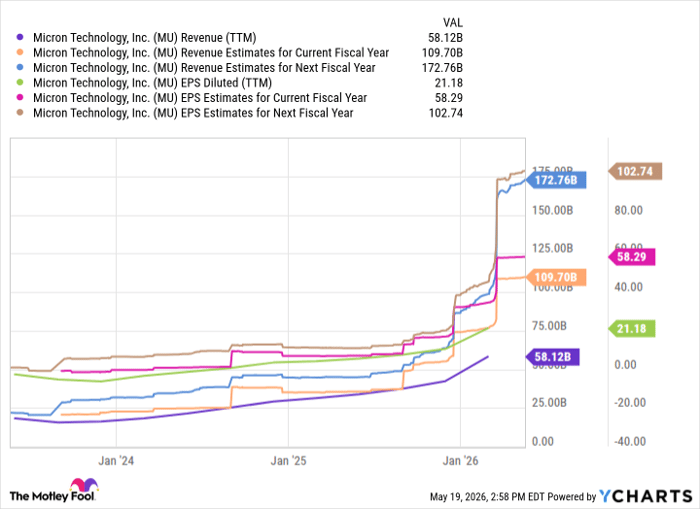

MU Revenue (TTM) data by YCharts.

Micron's focus on delivering higher-value products like HBM has translated into improving visibility from customer commitments, offering greater earnings stability. The company is investing heavily in next-generation HBM4E while also maintaining prudent financial discipline. In my view, Micron's rally appears sustainable in the medium term due to the multiyear runway of the AI infrastructure build-out.

The path to $1,500

Analysts project strong earnings growth for Micron over the next couple of years. For its fiscal 2027, which will begin in late August, earnings projections climb significantly toward $103 as production scales and pricing dynamics remain favorable. At current trading levels, Micron's forward price-to-earnings (P/E) multiple of about 12 appears attractive.

Simple math shows that applying a 15x multiple to a $103 fiscal 2027 EPS target results in a share price of about $1,500. Such a move would represent roughly 105% upside from Micron's current price of around $730.

While it's ambitious, I think my scenario aligns with the company's earnings trajectory should AI adoption continue at its current rapid pace and Micron maintain a competitive edge. In fact, I think there is a solid chance that Micron will outperform Wall Street's estimates.

There's growing conviction among investors that the AI memory boom is here to stay. So while predicting this level of stock price appreciation may appear aggressive, I think it is justifiable for a company that boasts sustained demand from hyperscalers and has a proven ability to build out its production capacity.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $477,813!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,320,088!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 24, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

Recommended Articles